English

English

Best No Annual Fee Cashback Cards: The 2026 Strategy Guide

In the 2026 economy, every dollar of your personal cash flow needs to be optimized. While premium travel credit cards with $600+ annual fees dominate the glossy marketing campaigns, they carry a hidden risk: if you don’t travel enough to offset the fee, you are actively losing money.

The foundation of a bulletproof personal finance strategy is built on no annual fee cashback cards.

The mathematical beauty of a no-fee card is simple. Because the sticker price is $0, your Effective Annual Fee (EAF) is zero. From the very first swipe, every cent of cashback you earn is pure, unadulterated profit. Whether you are funding daily logistics or building a travel fund, these cards offer liquidity and simplicity without the stress of “breaking even.”

Here is an analytical breakdown of the best no-fee cashback cards dominating the North American markets in 2026, separated by their strategic strengths.

Table of Contents

- The 2% Standard: Flat-Rate Powerhouses (US)

- The Optimizers: Rotating & Category Specialists (US)

- The Northern Advantage: Top Canadian Options

- Strategic Playbook: The “Two-Card Wallet” System

- Expert Insight: The Interest Rate Trap

- Frequently Asked Questions (FAQ)

1. The 2% Standard: Flat-Rate Powerhouses (US)

If you hate tracking spending categories and just want a simple, high-yield return on every purchase—from car insurance to dental bills—you need a flat-rate card. In 2026, the industry standard for a top-tier flat-rate card is 2%.

Wells Fargo Active Cash® Card

- The Reward: Unlimited 2% cash rewards on purchases.

- Why it Wins in 2026: It is arguably the most straightforward card on the US market. There are no categories to track and no quarterly activations. It also frequently offers a competitive $200 cash rewards welcome bonus after hitting a low minimum spend in the first three months, which is essentially free money for a no-fee card.

Citi Double Cash® Card

- The Reward: 2% cash back (1% when you buy, plus 1% as you pay for those purchases).

- Why it Wins in 2026: The Citi Double Cash is legendary for a reason. It gamifies responsible financial behavior by rewarding you for paying your bill. In 2026, Citi has also made it easier to convert this cashback into ThankYou Points, giving you a bridge into travel rewards later if your strategy evolves.

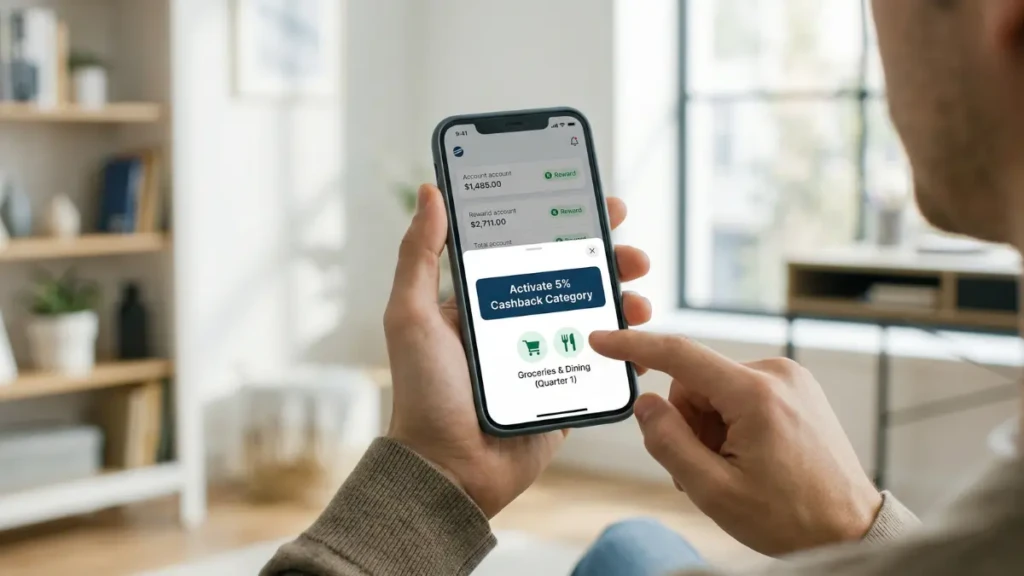

2. The Optimizers: Rotating & Category Specialists (US)

If you are willing to put in a little effort, category cards offer significantly higher returns (often 3% to 5%) on the things you buy most, like groceries, dining, and gas.

Chase Freedom Flex®

- The Reward: 5% cash back on up to $1,500 in combined purchases in bonus categories each quarter you activate, plus 3% on dining and drugstores.

- Why it Wins in 2026: The Freedom Flex is an optimizer’s dream. The 5% rotating categories often include high-spend logistics like Amazon, grocery stores, or gas stations. Furthermore, if you ever decide to upgrade to a premium Chase Sapphire card, you can pool these cashback points and convert them into high-value travel miles.

Capital One Savor Cash Rewards Credit Card

- The Reward: 3% cash back on dining, entertainment, popular streaming services, and at grocery stores.

- Why it Wins in 2026: Capital One recently dropped the annual fee on the Savor card, making it a dominant force for lifestyle spending. If a large portion of your monthly budget goes toward restaurants, concerts, or groceries, an unlimited 3% return with no annual fee is incredibly tough to beat.

3. The Northern Advantage: Top Canadian Options

The Canadian credit card market operates differently, with lower interchange fees making flat 2% no-fee cards rare. However, the category multipliers are incredibly strong for daily spenders.

Tangerine Money-Back World Mastercard

- The Reward: 2% cash back in two categories of your choice (three if you deposit the rewards into a Tangerine Savings Account), and 0.5% on everything else.

- Why it Wins in 2026: This is the ultimate customizable card. You get to choose your 2% categories from a list that includes Groceries, Gas, Recurring Bill Payments, and Restaurants. If your spending habits change (e.g., you start driving more), you can easily switch your categories in the app.

BMO CashBack® Mastercard®

- The Reward: 3% cash back on groceries, 1% on recurring bill payments, and 0.5% on everything else.

- Why it Wins in 2026: With food inflation still a factor in 2026, a no-fee card that offers 3% on groceries is a massive defensive asset for Canadian households. It is accessible to beginners and provides immediate relief at the checkout counter.

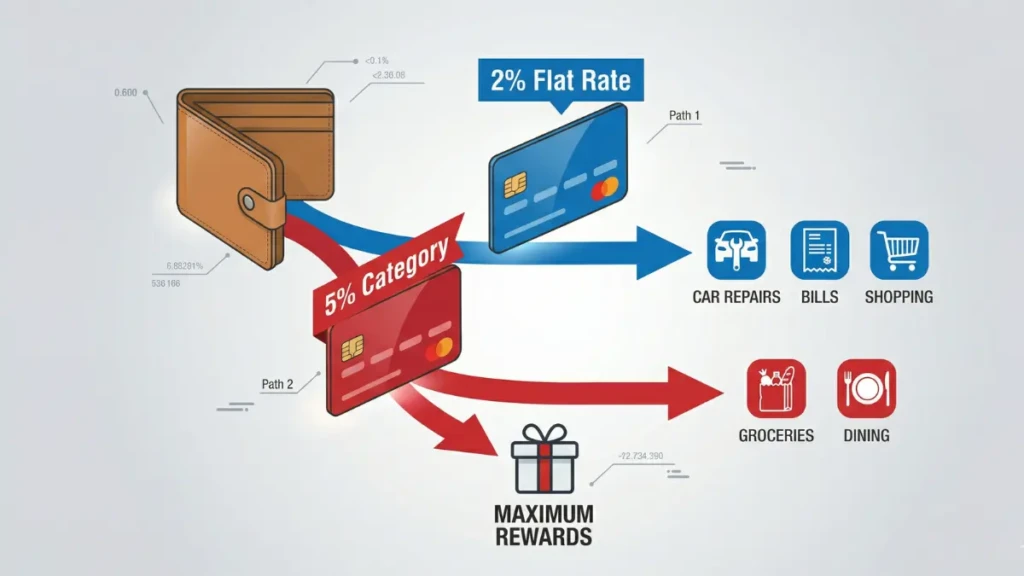

4. Strategic Playbook: The “Two-Card Wallet” System

To maximize your yield without complicating your life, employ the Two-Card System:

- The Anchor: Get a flat-rate 2% card (like the Wells Fargo Active Cash). Use this for “uncategorized” spending—medical bills, car repairs, online shopping, and taxes.

- The Multiplier: Get a category specialist (like the Capital One Savor or Tangerine Money-Back). Use this only for the specific categories where it earns 3% or 5% (like dining or groceries).

By splitting your spending, you ensure that every dollar you spend is earning the absolute maximum return possible, all while paying $0 in bank fees.

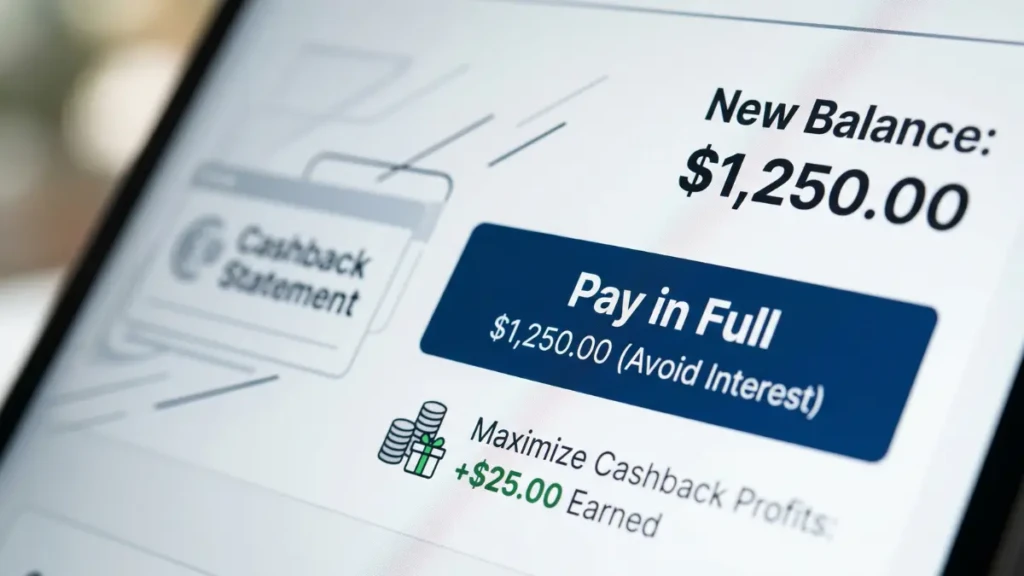

Expert Insight: The Interest Rate Trap

We asked a senior financial planner what the biggest mistake consumers make when pivoting to a cashback strategy.

“The moment you carry a balance, the math explodes. No annual fee cashback cards generally have variable APRs ranging from 20% to 29%. If you earn 2% cash back on a $1,000 purchase, you gained $20. If you don’t pay that balance in full and get hit with 25% interest, you just lost $250 over the year to earn that $20. Cashback is only profitable if you treat the credit card exactly like a debit card and pay the statement balance in full every single month.”

Frequently Asked Questions (FAQ)

What are the benefits of a no-fee credit card?

The primary benefit is zero overhead cost. You do not have to calculate an “Effective Annual Fee” or worry about spending a certain amount just to break even. It provides risk-free rewards, helps build your credit history for free, and acts as a financial safety net that costs nothing to keep open year after year.

How do I choose the right credit card with no annual fee?

Audit your monthly budget. Look at your top three expenses (usually rent, groceries, and dining/transportation). If your spending is heavily concentrated in one area like groceries, pick a card with a high category multiplier (like 3% or 5%). If your spending is erratic and spread across many random categories, a flat 2% card is the mathematically superior choice.

Can I use more than one lifetime-free credit card?

Absolutely. Utilizing multiple no-fee cards is the core of the “Two-Card Wallet” strategy. Because there are no annual fees, holding two or three cards costs you nothing and allows you to optimize your cashback across different spending categories. Just ensure you are paying all balances in full.

Do no annual fee cards have higher interest rates?

Generally, yes. Credit card issuers make their money either through annual fees, merchant transaction fees, or interest charges. Because they aren’t charging you an annual fee, the Annual Percentage Rate (APR) on unpaid balances is often very high. This is why paying the balance in full is mandatory for this strategy to work.

Optimize Your Checkout

In the world of personal finance, simplicity is often the ultimate sophistication. No annual fee cashback cards remove the anxiety of annual bank charges and guarantee that your rewards are working for you, not the other way around. Audit your spending, pick the card that aligns with your lifestyle, and start clawing back a percentage of your daily expenses.

Want to understand how these cards impact your overall credit profile? Review our guide on [How to Build Credit from Scratch: The 2026 Fast-Track Guide].