English

English

Building Credit from Scratch: A Step-by-Step Guide for New Immigrants in Canada and the USA

You arrive in a new country. You have savings in the bank, a job offer in hand, and big plans for your future. But when you try to rent an apartment, lease a car, or even set up a basic post-paid cell phone plan, you hit a brick wall.

“We need to run a credit check.”

It is the ultimate newcomer Catch-22: you need credit to survive in North America, but no one wants to give you credit until you already have a history. If you are struggling with building credit from scratch, take a deep breath. You are not alone, and this system is entirely hackable if you know the rules.

For new immigrants in both the US and Canada, establishing a financial footprint is your first major milestone. Let’s break down exactly how the timeline works, demystify secured versus unsecured cards, and look at the absolute best entry-level credit cards designed specifically for newcomers.

Table of Contents

- The Immigrant Credit Catch-22 (And How to Break It)

- Secured vs. Unsecured Credit Cards: The Key Differences

- The First 12 Months: Your Credit Building Timeline

- Top 3 Entry-Level Credit Cards for New US Immigrants

- Top 3 Entry-Level Credit Cards for Newcomers to Canada

- Expert Insight: Non-Negotiable Rules for Your First Year

- Frequently Asked Questions (FAQ)

The Immigrant Credit Catch-22 (And How to Break It)

In North America, your financial reputation is tracked by private companies called credit bureaus (primarily Equifax, TransUnion, and Experian). They compile a report card of how well you handle borrowed money, generating a three-digit number known as your credit score.

The problem? Credit history almost never crosses borders. You could have a flawless 15-year mortgage history in the UK, India, or Brazil, and the moment you step off the plane in Toronto or New York, your score is effectively zero.

To break this cycle, you need a financial institution willing to take a chance on a “thin file” (a profile with no history). This is where understanding the type of credit card you apply for becomes critical.

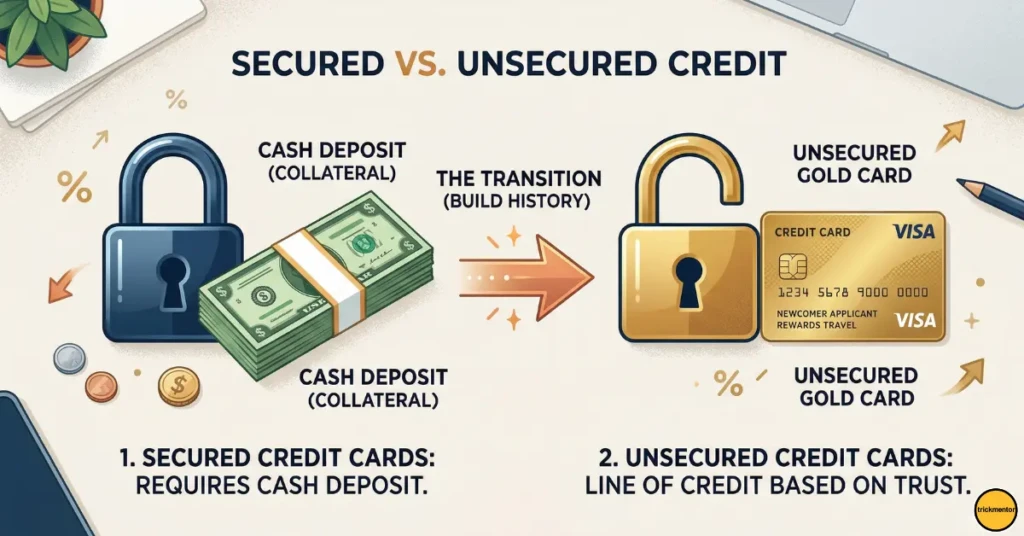

Secured vs. Unsecured Credit Cards: What’s the Difference?

When you apply for your first “new immigrant credit card,” you will face two distinct categories. Understanding this difference is the secret to getting approved on your first try.

Unsecured Credit Cards

This is the standard credit card. The bank issues you a line of credit based on their trust in your ability to repay.

- The Catch: Without a credit history, traditional banks will almost always auto-reject you for these cards.

- The Exception: Specific “Newcomer Packages” at major Canadian banks, or specialized US fintech companies that use alternative data (like your banking history from your home country).

Secured Credit Cards

This is the ultimate stepping stone for building credit from scratch.

- How it works: You provide a cash deposit upfront. If you put down a $500 deposit, your credit limit is $500.

- Why it matters: Because your own money protects the bank, approval is almost guaranteed. You use the card to buy groceries, pay it off every month, and the bank reports your good behavior to the credit bureaus. After 6 to 12 months, the bank refunds your deposit and upgrades you to an unsecured card.

Common Mistake: Avoid prepaid debit cards. While they look like credit cards and require cash upfront, they do not report your activity to the credit bureaus. They will not help you build credit.

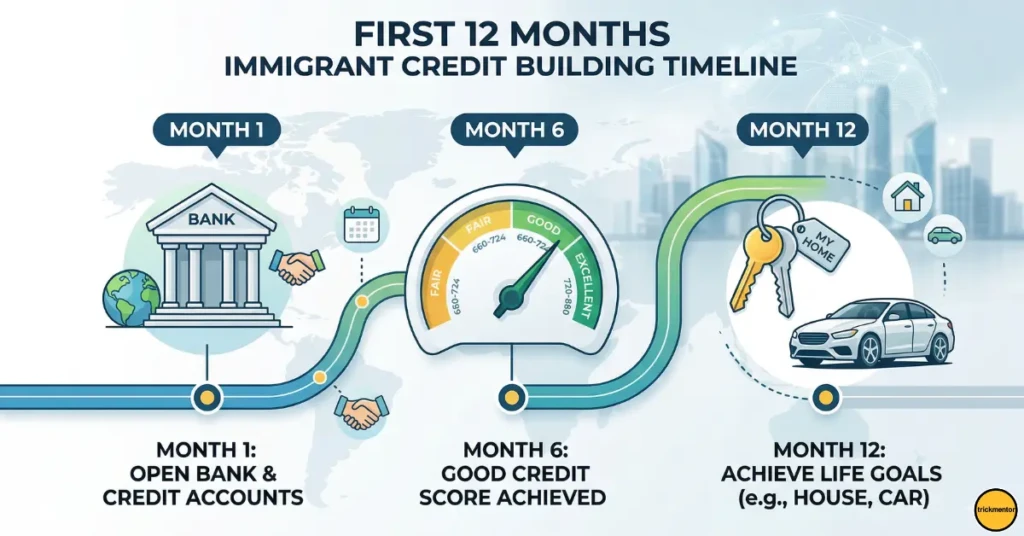

The First 12 Months: Your Credit Building Timeline

Building trust takes time. Here is what your first year should look like:

- Month 1 (Arrival): Open a local bank account. Apply for a newcomer-specific unsecured card or a secured credit card immediately.

- Months 2–5 (The Grind): Use your new card for small, predictable expenses (like groceries or a Netflix subscription). Pay the balance in full, three days before the due date.

- Month 6 (The Milestone): Your credit score officially generates. You should now be sitting in the “Fair” to “Good” range (around 650–680).

- Months 7–12 (Scaling Up): You can now apply for a second credit card, perhaps one that offers cash-back or travel rewards, or request a credit limit increase on your first card.

Need help managing your new cash flow? Read our guide on [Internal Link: Budgeting Strategies for Your First Year Abroad] to set yourself up for success.

Top 3 Entry-Level Credit Cards for New US Immigrants

The US system is heavily reliant on the Social Security Number (SSN). If you don’t have one yet, traditional banks will block your application. Fortunately, the landscape is shifting.

1. American Express (Via Nova Credit)

American Express has partnered with a service called Nova Credit, which translates your international credit history from countries like the UK, Australia, India, Mexico, and Canada into a US-equivalent score.

- The Big Win: You can get approved for premium unsecured cards (like the Blue Cash Everyday® Card) before you even get your SSN, leveraging the hard work you did in your home country.

2. Capital One Platinum Secured

If you cannot use Nova Credit, this is the gold standard for building credit from scratch.

- The Big Win: It requires no minimum credit score. Unlike many secured cards that require a deposit equal to your limit, Capital One might give you a $200 limit for a deposit of just $49, $99, or $200, depending on your application.

3. Petal 2 “Cash Back, No Fees” Visa

Petal is a fintech company that completely bypasses the traditional credit score model.

- The Big Win: Instead of a credit check, they link to your bank account to analyze your cash flow, income, and bills. If you have a solid income, you can get an unsecured card with limits up to $10,000, no SSN required (though an ITIN helps).

Top 3 Entry-Level Credit Cards for Newcomers to Canada

Canada is generally much friendlier to new immigrants when it comes to banking. The “Big Five” banks have aggressive programs to capture newcomer business, meaning you can often skip secured cards entirely.

1. Scotiabank StartRight® Program

Scotiabank is famous for its newcomer integration. Through the StartRight program, permanent residents, international students, and foreign workers can get approved for an unsecured credit card with limits up to $15,000 CAD.

- Top Pick: The Scotia Momentum® No-Fee Visa, which gives you cash back on groceries without an annual fee.

2. RBC Newcomer Advantage

RBC makes it incredibly easy to get your first piece of plastic without a Canadian credit history.

- Top Pick: The RBC Cash Back Mastercard. It’s an unsecured card that helps you build your Equifax and TransUnion files immediately while earning up to 2% cash back on groceries.

3. CIBC Welcome to Canada Program

CIBC offers a dedicated stream for immigrants who have been in Canada for less than 5 years.

- Top Pick: The CIBC Dividend® Visa. It has no annual fee, provides cash back on daily spending, and CIBC is excellent at automatically increasing your credit limit once you prove your reliability after the first 6 months.

If you are debating which country offers better financial prospects, review our breakdown on [Internal Link: US vs. Canada: Cost of Living and Earning Potential in 2026].

Expert Insight: 3 Non-Negotiable Rules for Your First Year

Building a credit score is like building a house: the foundation must be perfect. If you follow these three rules, you will be in the 700+ club within a year.

- Never Miss a Payment: Payment history makes up 35% of your credit score. Set up autopay immediately. A single missed payment can wreck a thin file.

- Keep Utilization Under 30%: Your “credit utilization” is how much of your limit you use. If you have a $1,000 limit, never let the statement balance cross $300. If you need to spend more, pay it off mid-month before the statement prints.

- Don’t Apply for Everything: Every time you apply for a credit card, the bank does a “hard pull” on your file, temporarily lowering your score. Pick one card, get approved, and don’t apply for another one for at least six months.

🔥 Frequently Asked Questions (FAQ)

What is a good credit score for a new immigrant? When you start, you have no score. After six months of on-time payments, a good starting target is between 650 and 680. Anything above 720 is considered excellent and will unlock premium financial products.

How to get a credit card without an SSN in the US? You can use an Individual Taxpayer Identification Number (ITIN), or apply with companies that use alternative data. Amex (via Nova Credit), Petal, and TomoCredit all offer pathways for immigrants without a Social Security Number.

Is it worth paying an annual fee on my first credit card? Generally, no. When building credit from scratch, your goal is simply to establish a history. Stick to no-annual-fee secured or unsecured cards. Save the annual fees for premium travel cards once your score is established.

Can I use my home country’s credit history in Canada or the US? In Canada, no. You must start entirely from scratch. In the US, Nova Credit allows immigrants from select countries to port their history over to apply for specific American Express cards.

Ready to Build Your Financial Future?

The initial frustration of the credit system is temporary. By selecting the right entry-level card and treating your spending with discipline, you are doing more than just building a score—you are building leverage. Pick a card from the list above, make your first small purchase, and start laying the foundation for your new life today.

Want more strategies for thriving in a new country? [How to Avoid Foreign Transaction Fees: Best US & Canadian Credit Cards (2026)] or read [External Link:Cashback vs Rewards Credit Cards: Which Is Better in 2026?] to stay ahead of the curve.

Best Travel Credit Cards in the USA 2026 — Hidden Gems

09th Apr 2026[…] Building Credit from Scratch: A Step-by-Step Guide for New Immigrants […]

Tax Strategies for US Digital Nomads and Freelancers in 2026

11th Apr 2026[…] Building Credit from Scratch: A Step-by-Step Guide for […]