English

English

How to Maximize Cash-Back Apps for Groceries in the USA & Canada

We have all experienced the checkout counter shock. You run in for a few basic ingredients, the cashier scans your items, and the total on the screen makes your stomach drop. With grocery inflation remaining stubbornly high in 2026, the days of casually tossing items into your cart without looking at the price tag are over.

If you are looking for ways to fight back against rising food costs, learning how to maximize cash-back apps for groceries is your most powerful weapon.

Forget the outdated image of extreme couponers spending hours cutting up Sunday newspapers. Today’s grocery savings happen digitally, instantly, and automatically. By using a specific combination of smartphone apps and high-yield credit cards, you can easily shave 10% to 15% off your monthly grocery bill in both the United States and Canada.

Let’s break down the exact strategy to stack your savings, compare the heavy-hitting apps like Ibotta and Checkout 51, and turn your discarded receipts into a steady stream of passive income.

Table of Contents

- The Secret Sauce: The “Triple Stack” Strategy

- Top 3 Cash-Back Grocery Apps in the USA

- Top 3 Cash-Back Grocery Apps in Canada

- The Credit Card Multiplier

- Common Mistakes to Avoid

- Expert Insight: Valuing Your Time

- Frequently Asked Questions (FAQ)

The Secret Sauce: The “Triple Stack” Strategy

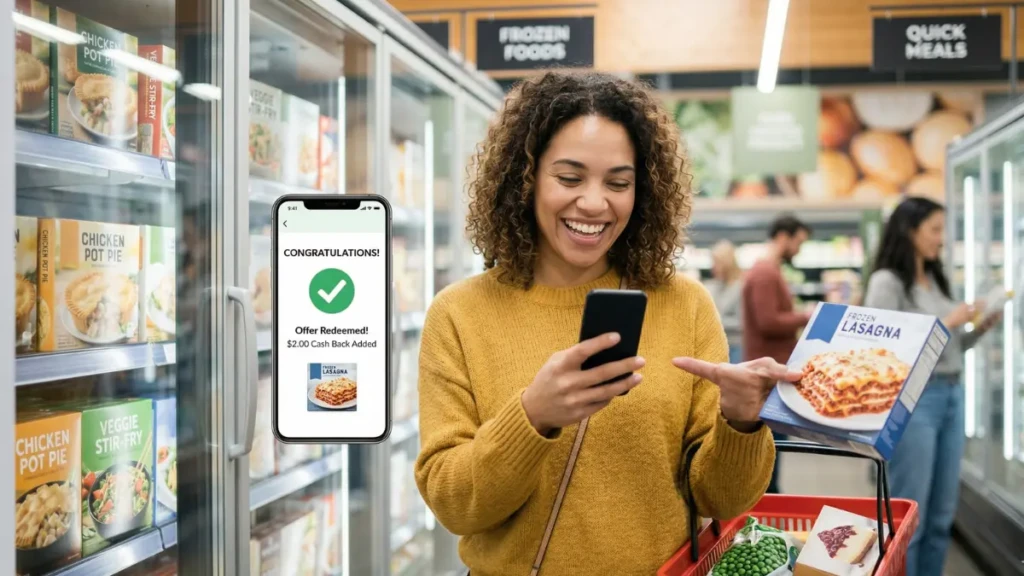

Most people download a single cash-back app, scan a receipt, earn fifty cents, and get bored. That is not how you win the game. The true value comes from “stacking.”

Stacking is the process of earning multiple different rebates on the exact same grocery transaction. A highly optimized grocery run in 2026 looks like this:

- Layer 1: The Store Loyalty Program. You scan your store card (like Kroger Plus in the US or PC Optimum in Canada) at the register to get the baseline member discounts.

- Layer 2: The Credit Card. You pay for the groceries using a credit card specifically optimized for supermarket spend, automatically earning 4% to 6% cash back.

- Layer 3: The Receipt Apps. You get to your car, take a picture of your receipt, and upload it to two or three different cash-back apps that don’t share data with each other.

You just turned a simple $100 grocery run into $12 worth of combined rewards. Do that every week, and you are putting $600 a year back into your pocket.

Top 3 Cash-Back Grocery Apps in the USA

The American market is saturated with rebate apps, but only a few consistently offer high-value returns on everyday essentials.

1. Ibotta (The Heavyweight Champion)

Ibotta remains the undisputed king of US grocery rebates. Before you shop, you scroll through the app and “add” offers to your list. After shopping, you snap a photo of your receipt, and the cash is deposited into your account.

- The Big Win: They partner with massive brands. You will frequently find $1 to $3 cash back offers on items you were already planning to buy, like yogurt, bread, and coffee.

- Pro Tip: Link your store loyalty cards (like Walmart or Target) directly within the Ibotta app. The cash back will apply automatically without you needing to scan the physical receipt.

2. Fetch Rewards (The Easiest Option)

If Ibotta requires too much planning, Fetch is your alternative. You don’t need to pre-select offers. You just scan any receipt from any grocery store, and the app automatically awards you points based on participating brands.

- The Big Win: Zero friction. It takes three seconds to scan a receipt, and you get guaranteed minimum points just for uploading it, even if you didn’t buy a featured brand.

3. Upside (The Emerging Threat)

Originally known strictly as a gas cash-back app, Upside has aggressively expanded into groceries. They operate on a card-linked model. You claim an offer at a specific local grocery store in the app, pay with your linked credit card, and the cash back automatically tracks.

- The Big Win: No receipt scanning required. You can often earn 5% to 10% back on your entire basket size at participating independent or regional grocers.

Top 3 Cash-Back Grocery Apps in Canada

The Canadian landscape is slightly different. Due to stricter data privacy laws and a highly consolidated grocery sector (Loblaws, Empire, Metro), the apps here require a bit more strategy.

1. Checkout 51 (The Classic Staple)

Born in Canada, Checkout 51 updates its offer list every Thursday morning. You select the items you want, buy them, and upload the receipt. Once your account hits $20, they mail you a physical check.

- The Big Win: They frequently offer “Any Brand” rebates. This means you can get 50 cents back on any brand of bananas, milk, or eggs, allowing you to save money even if you buy generic store brands.

2. Caddle (The Survey Hybrid)

Caddle is unique to Canada. Alongside standard grocery receipt uploads, they pay you small amounts (10 to 25 cents) to answer one-question surveys or watch 15-second ads.

- The Big Win: It is incredibly easy to hit the $20 payout threshold because you can interact with the app daily from your couch, supplementing your grocery scans with quick survey money.

3. Ampli (The Passive Earner)

Backed by RBC, Ampli is a card-linked app. You securely connect your Canadian debit or credit cards to the app. When you shop at a participating grocery or retail partner, the cash back is automatically credited to your Ampli account.

- The Big Win: It is “set it and forget it.” There are no receipts to scan. It works perfectly as a silent, background layer in your Triple Stack strategy.

The Credit Card Multiplier

You cannot fully maximize cash-back apps for groceries if you are paying with a debit card. You are leaving the biggest piece of the pie on the table.

For US Travelers: American Express Blue Cash Preferred®

This is widely considered the best grocery card in America. It offers a staggering 6% cash back at US supermarkets (up to $6,000 per year in purchases). If you max out that category, you are earning $360 a year before you even open a single receipt-scanning app.

For Canadian Travelers: Scotiabank Momentum® Visa Infinite*

In a market where 2% is the standard, this card dominates by offering 4% cash back on groceries and recurring bills. If you shop at Loblaws-owned stores, combining this card with your PC Optimum points creates a massive return on everyday spending.

Looking to optimize your overall budget? Dive into our comprehensive guide on [Internal Link: The 50/30/20 Budgeting Rule for 2026].

Common Mistakes to Avoid

- Buying Things You Don’t Need: This is the most dangerous trap. If you buy a $5 box of cookies just to get a $1 rebate on Ibotta, you didn’t save $1. You spent $4. Only clip offers for items already on your list.

- Letting Receipts Expire: Most apps require you to upload the receipt within 7 to 14 days of the purchase. Make it a habit to scan your receipts the moment you put your groceries in the trunk of your car.

- Ignoring the “Any Item” Offers: Don’t just look for big brand names. Many apps offer 10 cents just for uploading any receipt, regardless of what you bought. It adds up over a year.

Expert Insight: Valuing Your Time

We reached out to personal finance coach and extreme budgeter, Sarah Jenkins, to get her take on the 2026 app landscape.

“The biggest shift in grocery rewards right now is the move toward passive earning. Five years ago, you had to scan barcodes and manually verify purchases. Today, you must leverage card-linked offers. Link your primary grocery credit card to apps like Ampli or Upside. You do the work once, and the savings compound in the background for years without requiring an extra second of your time at the checkout counter.”

Frequently Asked Questions (FAQ)

Can I use the same receipt on multiple apps? Yes! This is the core of the stacking strategy. Unless the specific terms of an offer explicitly forbid it (which is rare), you can take the exact same grocery receipt and scan it into Ibotta, Fetch, and Checkout 51 simultaneously to earn rewards from all three companies.

Are cash-back apps safe to link to my bank account? Reputable apps like Ampli, Ibotta, and Rakuten use bank-level encryption and third-party services like Plaid to connect to your accounts. They never see your actual bank login credentials, only the transaction data needed to verify your purchases.

Do these apps work for online grocery delivery? Usually, yes. Apps like Ibotta and Fetch allow you to link your Instacart, Walmart Grocery, or Shipt accounts directly. Instead of scanning a physical paper receipt, the app pulls your digital e-receipt automatically.

Do I have to pay taxes on grocery cash back? In both the US and Canada, cash back earned from credit cards or rebate apps on personal purchases is generally considered a “discount” or a “rebate” rather than taxable income. You usually do not need to report it on your tax return.

Start Scanning and Start Saving

Fighting grocery inflation doesn’t require a radical lifestyle change; it just requires a slightly smarter checkout process. By combining a high-yield grocery credit card with a quick receipt scan in the parking lot, you can easily reclaim hundreds of dollars a year. Download two apps today, link your cards, and turn your next grocery run into a payday.

Want to save even more on daily expenses? Check out [ NerdWallet’s Best Grocery Credit Cards] to find the perfect card for your wallet, or read [The Penny Hoarder’s Guide to Couponing] for advanced strategies.

Ready to level up your travel game with your new savings? Read our guide on [Top 5 US & Canadian Cities for Digital Nomads in 2026 (Internet & Rent Rated)].

How to Plan a Luxury Vacation on a Middle-Class Income:

10th Apr 2026[…] How to Maximize Cash-Back Apps for Groceries in the USA […]