English

English

How to Improve Credit Score Fast in 2026 (Step-by-Step Guide)

You have found the perfect apartment, or perhaps you are finally ready to apply for that premium travel credit card to fund your next big trip. You check your credit score, and panic sets in. You are 30 points short of the “Excellent” tier, and applying right now means automatic rejection or a terrible interest rate.

The traditional advice from financial advisors is always the same: “Pay your bills on time and wait.” While that is true for long-term financial health, it is completely useless if you need to secure a loan this month.

If you need to know how to improve credit score fast, you have to stop treating your credit report like a mystery and start treating it like an algorithm. In 2026, the credit scoring models (FICO 8 and FICO 10T) respond incredibly well to specific, targeted actions.

Here is the exact step-by-step guide to legally and strategically increase credit score numbers in as little as 30 to 45 days.

Table of Contents

- Step 1: Master the “Statement Date” Utilization Hack

- Step 2: Request a Soft-Pull Credit Limit Increase

- Step 3: The Authorized User Shortcut (Piggybacking)

- Step 4: Inject Alternative Data (Rent & Bills)

- Step 5: Dispute Errors & Use Rapid Rescoring

- Expert Insight: Do Not Close Old Accounts

- Frequently Asked Questions (FAQ)

Step 1: Master the “Statement Date” Utilization Hack

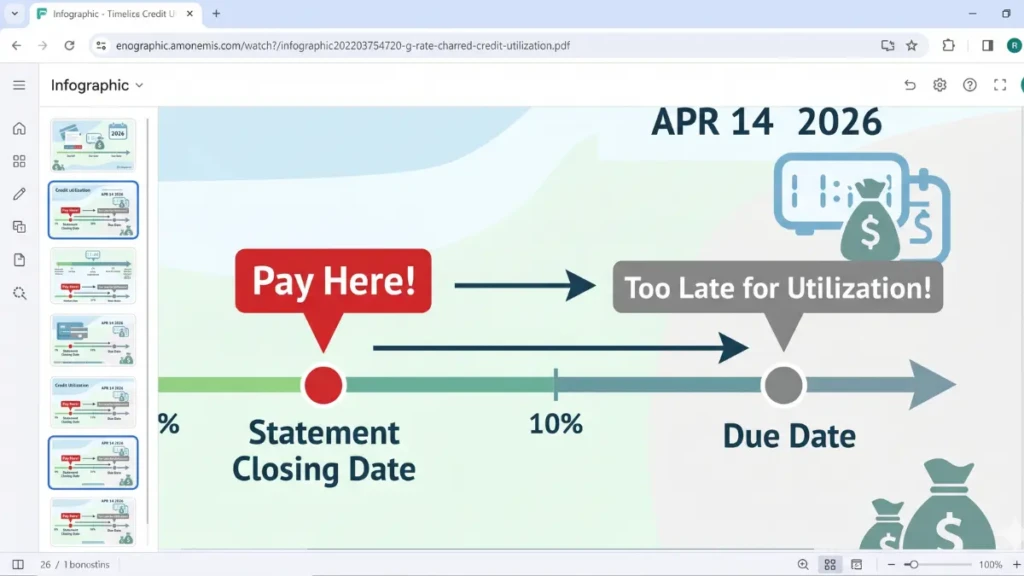

Your Credit Utilization Ratio (how much credit you are using compared to your total limit) makes up 30% of your total credit score. This is the fastest metric you can manipulate.

Most people think paying their bill in full on the “Due Date” is enough. It isn’t.

Credit card companies report your balance to the bureaus on your Statement Closing Date, which usually happens 21 days before your actual due date. If you spend $4,000 on a card with a $5,000 limit, the bank reports a massive 80% utilization to the bureaus, tanking your score—even if you pay it all off three weeks later on the due date.

The Fast Fix:

- Log into your banking app and find your “Statement Closing Date.”

- Pay your balance down to between 1% and 5% roughly three days before the statement closes.

- When the statement closes, the bank will report a tiny utilization ratio. You will see an immediate jump in your score within 30 days.

Step 2: Request a Soft-Pull Credit Limit Increase

If you do not have the extra cash to aggressively pay down your balances before the statement date, you can approach the math from the other side.

Credit utilization is: (Total Balances ÷ Total Limits) x 100.

If you cannot lower the balance, you can increase the limit. Many major credit card issuers in 2026 allow you to request a Credit Limit Increase (CLI) directly through their mobile app.

The Strategy:

- Check online to confirm your specific bank does a “Soft Pull” (which does not hurt your credit) rather than a “Hard Pull” for limit increases. Amex, Capital One, and Discover are famous for soft-pull CLIs.

- If your limit jumps from $5,000 to $10,000, and your balance stays the same, your utilization ratio instantly drops in half. This translates to an immediate score boost.

Step 3: The Authorized User Shortcut (Piggybacking)

If you have a “thin file” (meaning you are young or new to the country) and need to improve credit score fast, this is the ultimate shortcut.

Find a highly trusted family member or partner who has an old credit card account with a flawless payment history and a high limit. Ask them to add you as an Authorized User.

Why it works: The moment you are added, the entire history of that specific account is imported onto your credit report. You instantly gain years of perfect on-time payments and a larger total credit limit. The primary account holder does not even need to give you the physical card; simply having your name on the account is enough to trigger the algorithmic boost.

Step 4: Inject Alternative Data (Rent & Bills)

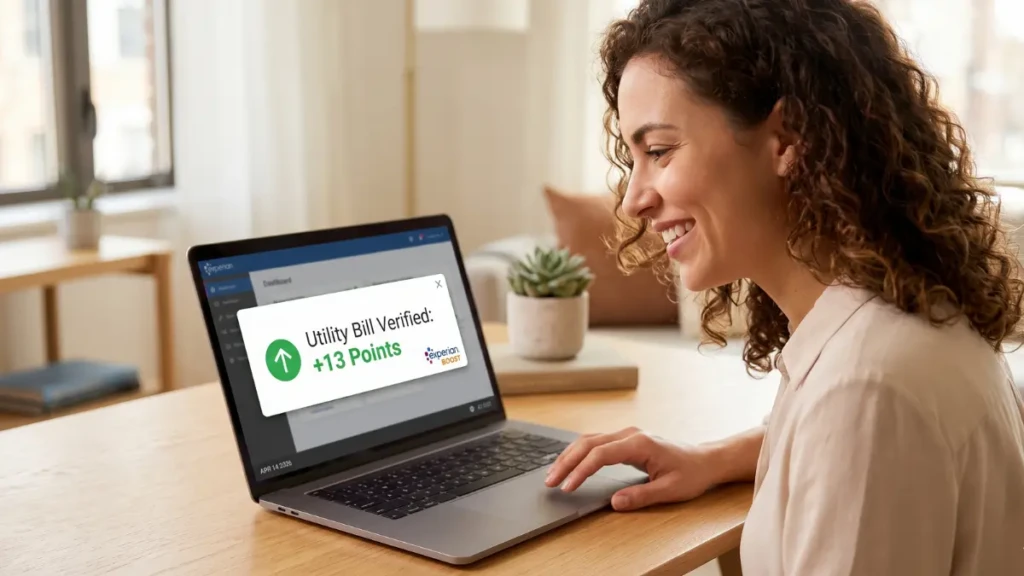

In the past, your Netflix subscription and electricity bill did nothing to increase credit score metrics. In 2026, you can force the bureaus to count them.

If you have a thin file or are rebuilding from past mistakes, use these tools to inject positive data immediately:

- Experian Boost: A free tool that scans your bank account for on-time utility, telecom, and streaming payments, injecting them directly into your Experian credit file. The average user sees a 13-point jump instantly.

- Rent Reporting: Ask your landlord to use a service like Boom or RentTrack, which reports your monthly rent payments to all three bureaus. Because rent is your largest expense, this establishes massive credibility with the scoring models.

Step 5: Dispute Errors & Use Rapid Rescoring

According to the FTC, 1 in 5 consumers has a verified error on their credit report dragging their score down.

Pull your free reports from AnnualCreditReport.com and look for misspelled names, late payments you actually paid on time, or collections accounts that you already settled. Dispute them immediately online. The bureaus have 30 days to investigate; if the creditor doesn’t respond, the negative mark is deleted.

The Mortgage Hack: Rapid Rescoring If you are applying for a mortgage and paid off a massive debt yesterday, you normally have to wait 30 to 45 days for your score to reflect it. Ask your mortgage broker to do a “Rapid Rescore.” For a small fee, the broker submits your proof of payment directly to the bureaus, forcing them to update your score in just 48 to 72 hours.

Expert Insight: Do Not Close Old Accounts

We consulted with a senior loan underwriter to uncover the biggest mistake people make when trying to clean up their credit profiles.

“People think closing their oldest, unused credit card ‘cleans up’ their file. In reality, it destroys your score. Closing an old card shortens your Average Age of Accounts (15% of your score) and lowers your total available credit, which ruins your utilization ratio. If a card has no annual fee, put a $5 recurring subscription on it, turn on auto-pay, and keep it open forever.”

Frequently Asked Questions (FAQ)

How fast can a credit score go up?

If you use the “Statement Date” hack to drastically lower your reported credit utilization, you can see your score jump by 20 to 50 points the moment the new balance is reported to the bureaus, which typically takes between 30 and 45 days.

Does paying off a collection account increase credit score?

It depends on the scoring model. Older models (like FICO 8) still penalize you for having the collection on your report, even if it is paid. However, the newer FICO 9 and FICO 10 models ignore paid collection accounts entirely. To be safe, always try to negotiate a “Pay for Delete” agreement with the collection agency before handing over any money.

How to increase credit score by 100 points in a month?

A 100-point jump in 30 days is only mathematically possible if you are correcting a massive negative factor. This usually happens in two scenarios: having a major error (like a false bankruptcy or false late payment) successfully disputed and deleted, or paying off maxed-out credit cards to drop your utilization from 100% down to 1%.

Does requesting my own credit report lower my score?

No. Checking your own credit score or pulling your own report is considered a “Soft Inquiry.” Soft inquiries do not affect your credit score at all. You can check your score on your banking app every single day without penalty.

Take Control of the Algorithm

You do not have to be a victim of a bad credit score. By understanding that the system is just an algorithm waiting for the right inputs, you can take immediate action. Pay your balances before the statement closes, leverage an authorized user account, and keep your old accounts open. With these aggressive tactics, you will be holding the keys to your new apartment or flying on premium travel rewards before the year is out.

Ready to leverage your newly improved score? Review our analytical guide on the [The Best Credit Cards in 2026: Cashback, Travel & No Annual Fee Options].

Related Post:

Building Credit from Scratch: Step-by-Step for US & Canadian

7 Mistakes That Destroy Your Credit Score (And How to Stop)

14th Apr 2026[…] How to Improve Credit Score Fast in 2026 (Step-by-Step Guide) […]

Venture X vs Sapphire Preferred: Which Is Better in 2026?

15th Apr 2026[…] How to Improve Credit Score Fast in 2026 (Step-by-Step Guide) […]

Debit vs Credit Card: The Hidden Truth (2026 Guide)

15th Apr 2026[…] How to Improve Credit Score Fast in 2026 […]

4 Things You Should Never Do to Your EV Battery (2026 Guide)

17th Apr 2026[…] How to Improve Credit Score Fast in 2026 […]