English

English

How to Use Credit Cards Smartly in 2026 (Zero Debt, Max Rewards)

In the modern financial ecosystem, a credit card is the ultimate double-edged sword. Wielded incorrectly, it is a wealth-destroying trap engineered to lock you into 25% to 30% Annual Percentage Rates (APR). Wielded correctly, it is a high-performance financial tool that acts as a secure firewall for your cash, builds an elite credit score, and generates hundreds of dollars in tax-free profit every year.

The difference between these two outcomes has nothing to do with your income level. It has everything to do with your system.

If you are treating your credit card like a short-term loan to buy things you cannot afford, you have already lost the game. To win in the 2026 economy, you must view your credit card strictly as a cash-flow optimization tool.

If you are ready to stop paying interest and start extracting massive value from banks, here is the bulletproof guide on how to use credit cards smartly to maximize your rewards and permanently avoid debt.

Table of Contents

- The Golden Rule: The “Debit Card” Mindset

- Mastering the Grace Period (Zero Interest Forever)

- The 10% Utilization Rule

- Maximizing Rewards: The ROI System

- Avoiding the 2026 BNPL Trap

- Expert Insight: The Automation Fail-Safe

- Frequently Asked Questions (FAQ)

1. The Golden Rule: The “Debit Card” Mindset

If you only remember one rule from this guide, make it this one: Treat your credit card exactly like a debit card.

A credit card is not an extension of your income. It is merely a secure gateway to spend the cash you already have sitting in your checking account.

- If you have $500 in your checking account, your true credit limit is $500, regardless of whether the bank gave you a $10,000 credit line.

- Before you swipe the card at a grocery store or checkout online, mentally verify that the cash is already in the bank to cover it. If it isn’t, you do not make the purchase. Period.

Adopting this mindset is the absolute foundation of learning how to avoid credit card debt.

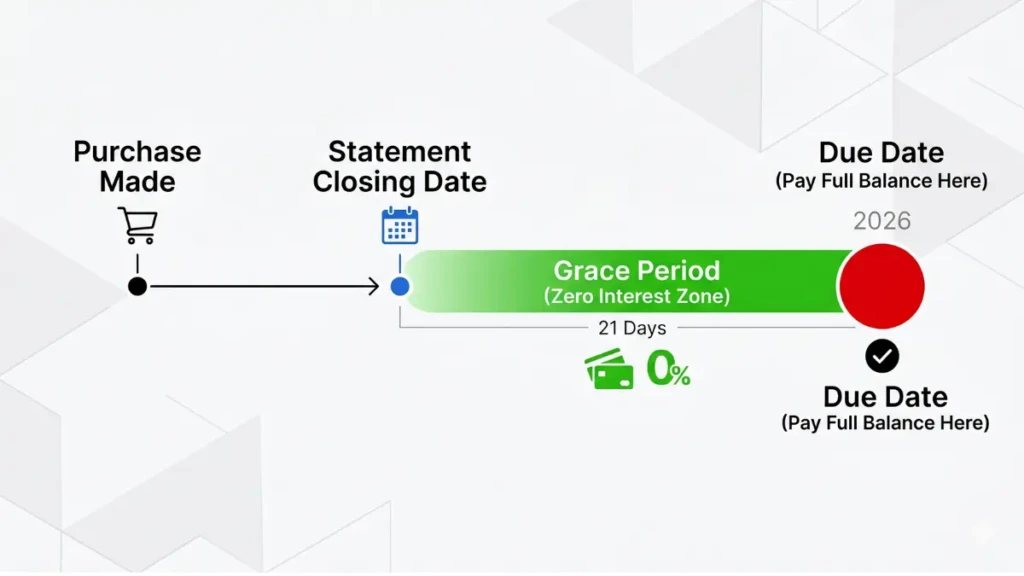

2. Mastering the Grace Period (Zero Interest Forever)

The biggest myth in personal finance is that carrying a small balance month-to-month improves your credit score. This is a toxic lie that only serves to make banks richer.

You never have to pay a single cent of interest to build an elite credit score if you understand the Grace Period. When your billing cycle closes, your bank sends you a statement. You typically have 21 to 25 days (the grace period) between the day that statement is generated and the actual “Due Date.”

The Strategy: Always, without exception, pay the Statement Balance in Full before the due date. Do not pay the “Minimum Balance.” Do not carry $50 over to the next month. If you pay the statement balance in full, the bank waives all interest charges. You get to borrow their money for 30 days for free, earn cash back on the purchase, and pay zero interest.

3. The 10% Utilization Rule

To use a credit card smartly, you must play the algorithm’s game. Your Credit Utilization Ratio (how much of your available limit you are using) makes up 30% of your FICO score.

While traditional advice says to keep this under 30%, the 2026 standard for elite borrowers is under 10%.

How to execute this: If you have a $5,000 limit, never let your reported statement balance exceed $500. If you need to make a $2,000 purchase, make the purchase to get the rewards, but log into your banking app and pay off $1,600 of it before the statement closing date. This ensures the bank only reports a tiny $400 balance to the credit bureaus, protecting your credit score from taking a hit.

4. Maximizing Rewards: The ROI System

Once you have the defensive habits in place, it is time to go on the offensive. A smart credit card user treats their daily spending as a predictable revenue system.

Do not settle for a basic 1% return. In 2026, you should be categorizing your major expenses and deploying the right card for the right job:

- The Anchor: Use a flat-rate 2% cashback card (like the Citi Double Cash or Wells Fargo Active Cash) for all random, un-categorized spending (mechanic bills, taxes, online shopping).

- The Multiplier: Use a category-specific card for your heaviest spending areas. If you spend heavily on food, use a card that earns 3% to 4% on groceries and dining (like the Capital One Savor or Amex Gold).

By putting every single daily expense on a card and paying it off instantly, you transform your existing living expenses into a high-yield ROI vehicle.

5. Avoiding the 2026 BNPL Trap

In 2026, nearly every major credit card app features a button next to your larger purchases that says something like “Split this into 6 monthly payments!” This is the banks adopting the “Buy Now, Pay Later” (BNPL) model.

Do not use this feature. While they often advertise a “fixed fee” rather than an APR, these installment plans artificially inflate your monthly fixed costs. It creates a psychological disconnect where you feel like you have more cash flow than you actually do, leading directly to lifestyle creep and, eventually, crushing debt. If you cannot pay for the item in full today, you do not buy it.

6. Expert Insight: The Automation Fail-Safe

We spoke with a performance wealth manager about the mechanics of failing safely.

“Human discipline is finite. You will eventually forget a due date because you are traveling, sick, or just busy. If you want to know how to use credit cards smartly, you must remove human error from the equation. The moment you activate a new credit card, set up ‘Auto-Pay for the Full Statement Balance’ drawn from your primary checking account. It acts as your ultimate fail-safe. Even if you completely forget the card exists, the system pays it off, avoiding late fees, protecting your score, and eliminating interest.”

Frequently Asked Questions (FAQ)

Does paying off a credit card early hurt your score?

No. Paying your balance early (before the statement closing date) lowers your credit utilization ratio, which actively boosts your score. However, you should leave a tiny balance (like $5 or $10) to post on the statement date so the credit bureaus see that the card is active, and then pay that remaining $10 before the actual due date.

How many credit cards should I have?

There is no magic number, but for most people, a “Two-Card Wallet” is the optimal balance of high ROI and low mental overhead. Have one card that acts as a flat-rate 2% catch-all, and a second card that acts as a multiplier for your highest spending category (like travel or groceries).

Should I ever take a cash advance from my credit card?

Absolutely never. A cash advance (using your credit card at an ATM to withdraw physical cash) is the worst transaction you can make. There is no grace period for cash advances—interest begins compounding the exact second the cash leaves the machine, and the APR is often 29% or higher, plus an upfront withdrawal fee.

Is it smart to close a credit card I don’t use anymore?

Closing an old credit card reduces your total available credit limit and shortens your average age of accounts, both of which will drop your credit score. Unless the card has a high annual fee that you are no longer getting value from, it is mathematically smarter to leave it open and put a small, automated $5 subscription on it to keep it active.

Command Your Cash Flow

You now have the exact blueprint for how to use credit cards smartly. By anchoring your habits with the “debit card mindset,” automating your full statement payments, and ruthlessly avoiding installment traps, you flip the script on the banking industry. The credit card is no longer a liability; it is your most powerful tool for building a predictable, high-yield financial foundation.

Ready to find the perfect card to execute this strategy? Head over to our deep dive on the [Best Everyday Credit Card 2026: Maximize Your Daily Spend] to find your ultimate daily driver.

Late Payment Credit Card: What Happens If You Miss a Payment?

15th Apr 2026[…] How to Use Credit Cards Smartly in 2026 (Zero Debt, […]

6 Hidden Credit Card Fees You Must Know (2026 Guide)

15th Apr 2026[…] How to Use Credit Cards Smartly in 2026 (Zero Debt, […]