English

English

Late Payment Credit Card: What Happens If You Miss a Payment?

We have all been there. You are managing a dozen different subscriptions, optimizing your cash flow, and suddenly you get a push notification that makes your stomach drop: you missed your credit card due date.

For those of us who obsess over maximizing rewards and optimizing financial systems, a missed payment feels like a catastrophic failure. However, before you panic and assume your borrowing power is ruined for the next decade, you need to understand how the banking algorithm actually treats a late payment credit card.

The consequences of missing a deadline depend entirely on how late the payment is. Being one day late is a minor administrative annoyance; being 30 days late is a full-blown financial crisis.

Here is the exact timeline of what happens when you miss a credit card payment in 2026, the penalties you will face, and the specific “Goodwill” strategy to fix the damage before it destroys your credit score.

Table of Contents

- Phase 1: 1 to 29 Days Late (The Financial Penalty)

- Phase 2: The 30-Day Mark (The Credit Score Disaster)

- Phase 3: 60+ Days Late (Penalty APR and Collections)

- Damage Control: How to Fix a Late Payment Instantly

- Expert Insight: The “Goodwill Adjustment” Script

- Frequently Asked Questions (FAQ)

1. Phase 1: 1 to 29 Days Late (The Financial Penalty)

If you miss your payment by 24 hours, take a deep breath. Your credit score is completely safe. By federal law, credit card issuers cannot report a late payment to the major credit bureaus (Experian, Equifax, TransUnion) until it is a full 30 days past due. However, your bank will exact its revenge through your wallet immediately.

What happens on Day 1:

- The Late Fee: You will be hit with an immediate late fee. (Note for 2026: While the CFPB attempted to cap these fees at $8 a few years ago, the rule was vacated by federal courts. Today, standard late fees typically hit the legal maximum of $30 to $41).

- Loss of the Grace Period: If you do not pay your statement balance in full, you immediately lose your interest grace period. The bank will start charging you their standard APR on your remaining balance, and on any new purchases you make, compounding daily.

2. Phase 2: The 30-Day Mark (The Credit Score Disaster)

This is the cliff. If your payment becomes exactly 30 days past due, your bank will trigger an automated report to the credit bureaus.

Because your Payment History makes up a massive 35% of your FICO algorithm, a 30-day late payment is one of the most destructive marks you can get on a credit profile.

The Damage:

- If you have an elite credit score (750+), the algorithm penalizes you harder than someone with a bad score. A single 30-day late payment can cause your score to plummet by 80 to 110 points overnight.

- This red flag will remain on your credit report for exactly seven years, signaling to future mortgage lenders and auto financiers that you are a high-risk borrower.

3. Phase 3: 60+ Days Late (Penalty APR and Collections)

If you ignore the bill for 60 days, the bank escalates from algorithm penalties to aggressive financial lockdowns.

- The Penalty APR: At 60 days late, the bank is legally allowed to trigger the “Penalty APR” hidden in your card’s terms and conditions. This instantly spikes your interest rate, often jumping from a standard 24% up to a punitive 29.99% or higher.

- Account Freeze: Your available credit line will be frozen or drastically reduced. You will no longer be able to swipe the card.

- Charge-Off (120-180 Days): If you still do not pay, the bank will “charge off” the debt. They close the account permanently and sell the debt to a third-party collection agency, devastating your credit score for the better part of a decade.

4. Damage Control: How to Fix a Late Payment Instantly

If you realize you missed your due date yesterday, drop everything and execute this sequence:

- Pay the Minimum Immediately: Do not wait until you have the cash to pay the full balance. Transfer the minimum payment right this second to stop the clock and prevent the 30-day reporting window from opening.

- Pay the Statement Balance (If Possible): To stop the “trailing interest” death spiral, pay the entire remaining statement balance so you can reset your grace period for the next cycle.

- Automate Your Defense: Go into your banking app and set up “Auto-Pay: Minimum Balance.” Even if you manually pay in full every month, having the minimum on auto-pay serves as a bulletproof fail-safe against future human error.

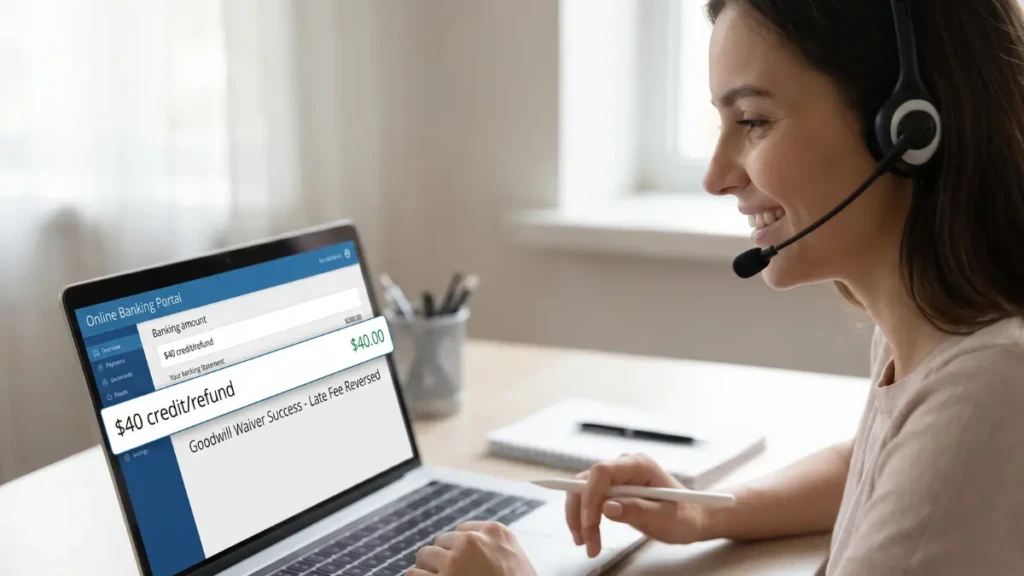

5. Expert Insight: The “Goodwill Adjustment” Script

If this is your first time missing a payment and you were hit with a $40 late fee, you can almost always get your money back. We use this exact script at https://www.google.com/search?q=trickmentor.com to help readers optimize their banking logistics.

Call the number on the back of your card and ask for a Goodwill Waiver:

“Hi, I noticed a late fee of $40 on my recent statement. I completely missed the notification, but I just went in and paid the balance in full today. I’ve been a loyal customer for [X years] and have never missed a payment before. Since this was an honest mistake that has already been corrected, can you please waive this late fee as a one-time courtesy?”

Banks empower their frontline customer service reps to waive one late fee every 12 to 18 months for accounts in good standing. If the first rep says no, politely hang up, call back, and ask a different representative.

Frequently Asked Questions (FAQ)

Can I get a 30-day late payment removed from my credit report?

It is extremely difficult, but not impossible. If the 30-day mark was legitimate, the credit bureaus will not remove it via a dispute. Your only option is to write a physical “Goodwill Letter” to the bank’s executive office, explaining any extenuating circumstances (e.g., hospitalization, natural disaster) and politely asking them to retroactively remove the report.

Does my interest rate go up if I am 1 day late?

No. By law, banks cannot impose a Penalty APR until your account is at least 60 days past due. However, you will be charged standard interest on your balance because you lost your interest-free grace period.

Will a late payment on a business credit card affect my personal credit?

It depends on the issuer. Most business credit cards (like Amex Business or Chase Ink) require a personal guarantee, but they do not report to your personal credit profile if the account is in good standing. However, if the account becomes 30 to 60 days late, almost all major issuers will pierce the corporate veil and report the severe delinquency to your personal credit file.

What time is my credit card payment actually due?

Do not assume you have until midnight. The exact cutoff time is buried in your cardholder agreement and varies by bank (e.g., 5:00 PM EST or 11:59 PM EST). If you pay at 10:00 PM, but your bank’s cutoff was 5:00 PM, your payment will be processed the following business day, triggering a late fee.

Set the Fail-Safe

A late payment credit card penalty is a tax on a broken system. You should never rely on your memory to manage your financial infrastructure. By setting up automated minimum payments today, you guarantee that you will never surrender your credit score to a simple scheduling error.

Want to make sure you are extracting the maximum ROI out of your credit cards? Read our master guide on [How to Use Credit Cards Smartly in 2026 (Zero Debt, Max Rewards)].

Rules To Follow: https://www.scotiabank.com/ca/en/personal/bank-your-way/digital-banking-guide/credit-cards/autopay.html