English

English

7 Mistakes That Destroy Your Credit Score (And How to Stop)

Building an excellent credit score takes years of discipline, patience, and strategic financial planning. Destroying it takes exactly 30 days.

In the 2026 financial landscape, where algorithms dictate your mortgage rates, your auto insurance premiums, and even your ability to rent an apartment, your three-digit FICO score is your most vital asset. Yet, millions of people unknowingly sabotage their financial profiles not through malicious intent, but through simple, easily avoidable bad credit habits.

If you have noticed a sudden, terrifying drop in your score, or if you are preparing to apply for a major loan, you cannot afford to trigger the algorithm’s penalty flags.

Here is the analytical breakdown of the 7 mistakes that destroy your credit score, the psychology behind why the bureaus penalize them so heavily, and exactly how to fix them.

Table of Contents

- The Fatal Flaw: The 30-Day Late Payment

- The Utilization Trap: Maxing Out Your Limits

- The “Clean Up” Myth: Closing Old Credit Cards

- The Desperation Signal: Applying for Too Much Credit

- The Empathy Trap: Co-Signing a Loan

- The Silent Killer: Ignoring Your Credit Report

- The Balance Transfer Spiral

- Expert Insight: The Collections Warning

- Frequently Asked Questions (FAQ)

1. The Fatal Flaw: The 30-Day Late Payment

Your payment history makes up a massive 35% of your total FICO score. It is the single most important metric in the entire algorithm.

If you pay your bill three days late, you will get hit with a late fee from your bank, but your credit score will not drop. The true damage occurs at the 30-day mark. If a payment becomes 30 days past due, the bank legally reports it to the credit bureaus (Experian, Equifax, TransUnion).

- The Damage: A single 30-day late payment can drop an excellent credit score by 80 to 100 points instantly.

- The Fix: Treat your credit card bills like your rent. Set up automatic minimum payments for every single credit card you own. Even if you manually pay the rest of the balance later, the auto-pay ensures you never cross that catastrophic 30-day threshold.

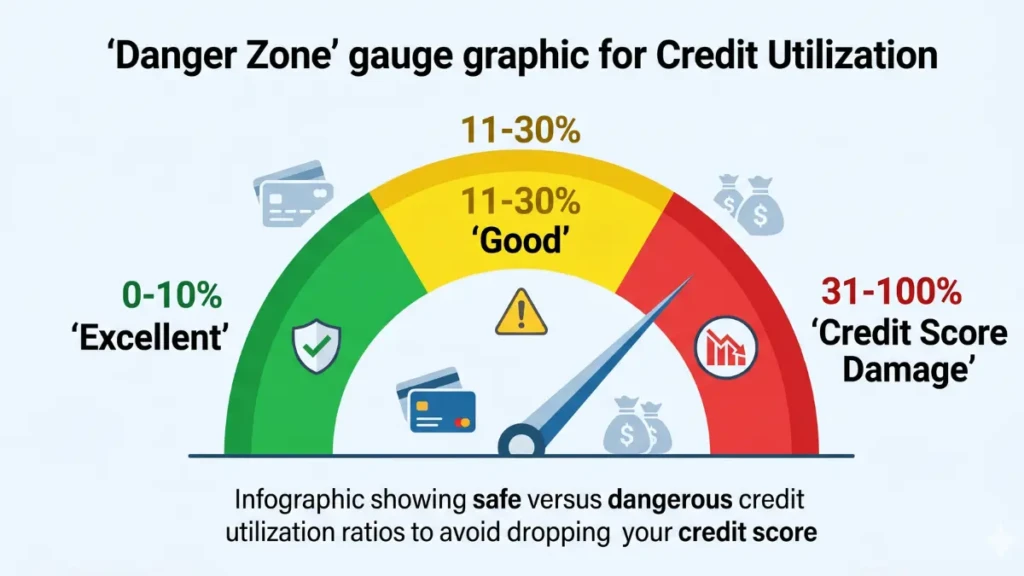

2. The Utilization Trap: Maxing Out Your Limits

Credit utilization—how much credit you are using compared to your total limit—accounts for 30% of your score.

One of the most common bad credit habits is treating your credit limit as a target rather than a safety net. If you have a $5,000 credit limit and spend $4,500, your utilization is 90%. To the algorithm, a 90% utilization ratio screams financial distress.

- The Damage: Maxing out a card can easily shave 40 to 60 points off your score.

- The Fix: Never let your statement balance exceed 10% to 30% of your total limit. If you have to make a large purchase, pay the balance down before your statement closing date so the bank reports a low number to the bureaus.

3. The “Clean Up” Myth: Closing Old Credit Cards

Many people attempting to embrace financial minimalism decide to close their oldest, unused credit cards. This is a massive mistake that hits you with a “double penalty.”

First, it shortens your “Average Age of Accounts” (15% of your score). The older your credit file, the more reliable you appear. Second, it destroys your utilization ratio by wiping out your available credit.

- The Damage: If you close a card with a $10,000 limit, your total available credit shrinks by $10,000. If you have balances on other cards, your overall utilization percentage instantly spikes, dragging your score down with it.

- The Fix: If an old card has no annual fee, put it in a drawer. Put a small $5 recurring subscription (like Spotify) on it and set it to auto-pay. Leave it open forever.

4. The Desperation Signal: Applying for Too Much Credit

Every time you formally apply for a new credit card, auto loan, or mortgage, the lender executes a “Hard Inquiry” on your credit report.

- The Damage: A single hard inquiry typically drops your score by 3 to 5 points. This is minor. However, if you apply for five credit cards in a single month because you are chasing sign-up bonuses or desperate for cash, you will accumulate five hard inquiries. The algorithm flags this as “credit-seeking behavior,” signaling that you are a high-risk borrower on the verge of bankruptcy.

- The Fix: Space out your credit applications. Wait at least 90 days (preferably 6 months) between applying for new credit cards.

5. The Empathy Trap: Co-Signing a Loan

When you co-sign a student loan for your child or an auto loan for a partner, you are legally telling the bank: “If they do not pay, I will.”

The moment you co-sign, that entire debt appears on your credit report. If your partner is 30 days late on their car payment, it counts as a 30-day late payment on your file. If the loan defaults, your credit is destroyed.

- The Fix: Never co-sign a loan unless you are fully prepared and financially able to make 100% of the payments yourself.

6. The Silent Killer: Ignoring Your Credit Report

Identity theft and bureau errors are rampant in 2026. The Federal Trade Commission reports that millions of consumers have verifiable errors on their credit profiles that artificially depress their scores.

If a hospital accidentally sends a paid $500 bill to collections, or if someone opens a fraudulent utility account in your name, it will wreck your score quietly in the background.

- The Fix: You are legally entitled to free weekly credit reports from AnnualCreditReport.com. Check your reports at least three times a year. If you see a false late payment or an account you do not recognize, dispute it online immediately.

7. The Balance Transfer Spiral

Balance transfer cards (offering 0% APR for 12-18 months) are excellent tools for paying down debt without interest. However, they breed toxic bad credit habits if used incorrectly.

Many consumers transfer their $5,000 balance to a new 0% card, freeing up the $5,000 limit on their old card. Feeling a false sense of financial relief, they start spending on the old card again. Twelve months later, they now owe $10,000.

- The Fix: If you do a balance transfer, you must freeze the old card in a block of ice (literally or metaphorically). You cannot use it again until the transferred debt is 100% eradicated.

Expert Insight: The Collections Warning

We asked a former credit underwriter what the most frustrating mistake they see in 2026 is.

“People let petty disputes ruin their financial lives. I see applicants with an 800 score drop to a 650 because they refused to pay a $75 final utility bill or a minor gym cancellation fee out of principle. The company sends that $75 to a collection agency, and a ‘Collections Account’ appears on their credit report. A collection mark is a massive red flag to any mortgage lender. Pay the $75, get the clean break, and protect your multi-million dollar borrowing power.”

Frequently Asked Questions (FAQ)

Does checking my own credit score lower it?

No. Checking your own credit score through a banking app, a free service like Credit Karma, or pulling your official report is considered a “Soft Inquiry.” Soft inquiries do not impact your credit score whatsoever. You can check your score every single day without penalty.

How long do late payments stay on my credit report?

A payment that is 30 days (or more) late will remain on your credit report for exactly seven years. However, its impact on your FICO score lessens over time. A late payment from last month will devastate your score, but a late payment from five years ago will only have a minor effect.

Will paying off a collection agency immediately fix my score?

With older scoring models (like FICO 8), paying a collection account does not remove the negative mark from your report; it simply changes the status to “Paid Collection,” which still hurts your score. Newer models (like FICO 9) ignore paid collections. To be safe, always try to negotiate a “Pay for Delete” agreement with the agency before you hand over the money.

Does a debit card build credit?

No. Debit cards use your own cash pulled directly from your checking account. Because you are not borrowing money, banks do not report debit card activity to the credit bureaus. You must use a credit card or a loan to generate a credit score.

Guard Your Financial Passport

Avoiding the mistakes that destroy your credit score is much easier than trying to rebuild one from the ashes. By automating your minimum payments, keeping your utilization aggressively low, and leaving your oldest accounts open, you build a resilient financial profile. Treat your credit score with the respect it deserves, and the entire banking system will open its doors to you.

Need to reverse the damage quickly? Read our step-by-step guide on [How to Improve Credit Score Fast in 2026 (Step-by-Step Guide)] to start manipulating the algorithm in your favor.

Related Post:

Credit Utilization Ratio Explained (The 2026 Master Guide)

14th Apr 2026[…] 7 Mistakes That Destroy Your Credit Score (And How to […]