English

English

Debit vs Credit Card: The Hidden Truth (2026 Guide)

For decades, traditional financial advice has preached a simple mantra: If you want to be financially responsible, cut up your credit cards and only use debit. On the surface, it makes sense. A debit card forces you to spend only the money you actually have, keeping you out of the terrifying spiral of high-interest debt. However, in the high-tech, highly digitized 2026 economy, this old-school advice is not just outdated—it is dangerously incomplete.

When you dive into the debit vs credit card debate, you uncover a hidden truth. The financial system is mathematically stacked against the debit card. By choosing to swipe debit at the grocery store or online, you are actively exposing your life savings to devastating fraud, missing out on hundreds of dollars in free cash flow, and keeping yourself invisible to the algorithms that dictate your financial future.

If you are ready to graduate from basic budgeting to strategic wealth protection, here is the unvarnished truth about how these two pieces of plastic actually work.

Table of Contents

- The Mechanical Difference: Whose Money Is It?

- The Hidden Truth #1: The Financial Firewall

- The Hidden Truth #2: The Opportunity Cost

- The Hidden Truth #3: The Credit Score Monopoly

- When SHOULD You Use a Debit Card?

- Expert Insight: The Psychology of Spending

- Frequently Asked Questions (FAQ)

1. The Mechanical Difference: Whose Money Is It?

To understand the hidden mechanics, you must first understand the fundamental flow of capital.

- The Debit Card (Your Money): When you swipe a debit card, you are opening a direct, unshielded pipeline into your personal checking account. The money is deducted immediately.

- The Credit Card (The Bank’s Money): When you swipe a credit card, you are using “Other People’s Money” (OPM). The bank pays the merchant on your behalf. You are essentially taking out a micro-loan for 30 days. You hold onto your own cash until your statement is due at the end of the month.

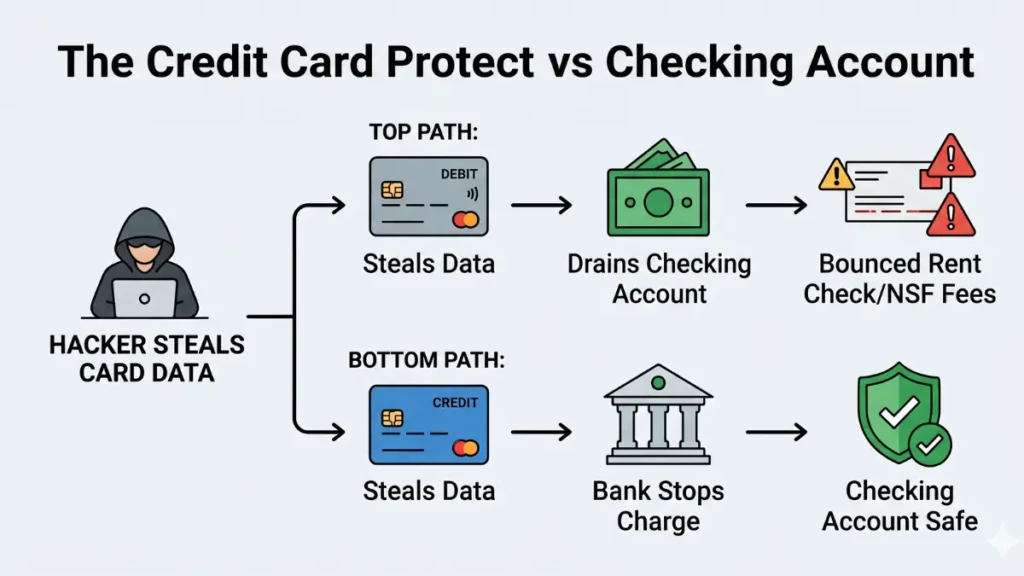

2. The Hidden Truth #1: The Financial Firewall

This is the most critical difference in the debit vs credit card comparison, and it comes down to federal law.

With AI-driven scams and sophisticated card skimmers at gas stations and ATMs in 2026, it is no longer a matter of if your card data will be stolen, but when.

The Debit Card Nightmare: Debit cards are protected by the Electronic Fund Transfer Act (EFTA). If a hacker steals your debit card number and drains $5,000 from your account, your actual money is gone. Your rent check will bounce, your car payment will fail, and you will be hit with overdraft fees. While the bank investigates (which can take weeks or months), your checking account remains empty. You are the victim.

The Credit Card Firewall: Credit cards are protected by the Fair Credit Billing Act (FCBA), which legally caps your liability for fraudulent charges at $50 (though almost all major issuers offer a $0 Liability Policy). If a hacker charges $5,000 to your credit card, they stole the bank’s money, not yours. Your checking account is untouched. You simply click “Dispute” on your app, the bank freezes the charge, and they fight the fraudsters with their own lawyers. A credit card is a financial firewall between the world and your life savings.

3. The Hidden Truth #2: The Opportunity Cost

Every time you swipe a debit card in 2026, you are leaving money on the table. This is the concept of Opportunity Cost.

Credit card companies charge merchants a “swipe fee” (interchange fee) of 2% to 3% on every transaction. To incentivize you to use their card, banks kick back a portion of that fee to you in the form of rewards, cash back, or travel points. Debit cards do not offer this (or offer microscopic fractions of a percent).

The 2026 Math: If your household spends $3,000 a month on daily logistics (groceries, gas, dining, bills):

- Using a Debit Card: You earn $0.

- Using a 2% Cashback Credit Card: You earn $60 a month, or $720 a year, in pure, untaxed profit.

By using a debit card, you are effectively paying full price while credit card users are getting a universal 2% discount funded by the merchants.

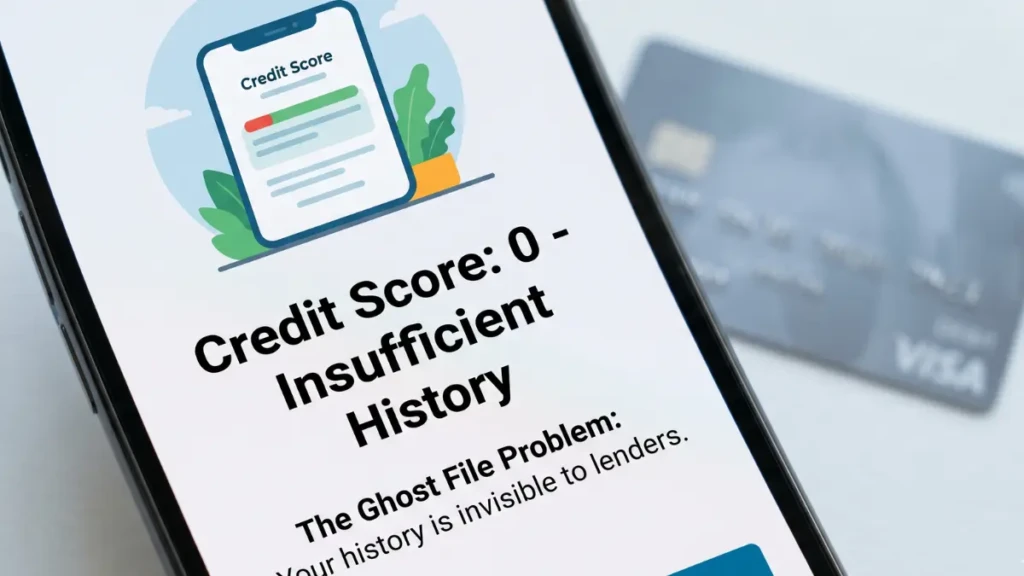

4. The Hidden Truth #3: The Credit Score Monopoly

In the North American economy, your three-digit credit score is your financial passport. It dictates your mortgage rate, your auto insurance premiums, and your ability to rent an apartment.

The hidden truth is that debit cards are financially invisible. Because a debit card uses your own cash, you are not borrowing anything. Therefore, banks do not report your debit card transactions to the credit bureaus (Experian, Equifax, TransUnion).

You could have a million dollars in your checking account and use your debit card flawlessly for ten years, and you would still have a “Ghost File” (a credit score of zero). To the algorithm, you are an unproven, high-risk entity. You must use a credit card (even a secured card) to generate the data required to build a 750+ credit score.

5. When SHOULD You Use a Debit Card?

Despite its flaws, the debit card still has two highly specific, necessary functions in your wallet:

- ATM Withdrawals: If you need physical cash, use a debit card. If you use a credit card at an ATM, it is processed as a “Cash Advance.” This triggers an immediate, massive fee (often 5% of the total) and begins accumulating sky-high interest the exact second the cash leaves the machine.

- Debt Recovery: If you lack financial discipline and currently carry thousands of dollars in high-interest credit card debt, the rewards and security of a credit card are mathematically destroyed by the 25% APR you are paying. In this scenario, you must lock your credit cards away and operate strictly on a debit card until your debt is eradicated.

Expert Insight: The Psychology of Spending

We consulted with a behavioral economist to understand why the debit card still holds such a grip on the public.

“The debit vs credit card debate is entirely psychological. Credit cards abstract the pain of paying. When you swipe a credit card, your bank account balance doesn’t immediately drop, which can trick the brain into overspending by 15% to 20% compared to cash or debit. The ‘Hidden Truth’ is that credit cards are the superior financial tool, but they require the discipline of a debit card user. If you can treat your credit card like a debit card—meaning you never swipe it unless the cash is already sitting in your checking account to pay it off—you win the game.”

Frequently Asked Questions (FAQ)

Can I rent a car or book a hotel with a debit card?

It is extremely difficult. Rental car agencies and hotels place “holds” (authorizations) on your card for incidentals. If you use a debit card, that hold freezes your actual cash in your checking account, preventing you from using it for days or weeks. Furthermore, many premium rental agencies flat-out refuse to accept debit cards due to the lack of collateral.

Does overdraft protection on a debit card help build credit?

No. Overdraft protection is simply a service where your bank covers a transaction if your account hits zero (usually for a steep fee). It is not a traditional line of credit and is not reported to the credit bureaus.

Can someone steal my money with contactless (tap-to-pay) debit cards?

Yes, though the risk of someone stealing your card data via an RFID scanner in public is statistically very low compared to online data breaches. However, if your physical card is stolen, thieves can easily use the “tap” feature for purchases under the PIN-limit threshold before you realize it is missing. This is why the credit card firewall is crucial.

Are there debit cards that give rewards in 2026?

Some fintech companies and neo-banks offer debit cards with 1% cash back or cryptocurrency rewards. While better than nothing, they still lag significantly behind the 2% to 5% multipliers offered by premium credit cards, and they still expose your primary account to EFTA liability rules rather than the superior FCBA protections.

Upgrade Your Financial Arsenal

The debit vs credit card debate is only a debate if you ignore the mechanics of the modern economy. A debit card is an excellent tool for accessing ATM cash, but swiping it at a merchant terminal is a massive strategic error. By locking your debit card in a drawer and using a credit card for your daily logistics, you immediately erect a bulletproof firewall around your cash, start building an elite credit score, and claw back hundreds of dollars a year in rewards.

Ready to find the perfect card to replace your debit habit? Read our analytical guide on the [Best Everyday Credit Card 2026: Maximize Your Daily Spend].

How to Use Credit Cards Smartly in 2026 (Zero Debt, Max Rewards)

15th Apr 2026[…] Debit vs Credit Card: The Hidden Truth (2026 Guide) […]

How to Improve Credit Score Fast in 30 Days (2026 Guide)

23rd Apr 2026[…] Debit vs Credit Card: The Hidden Truth (2026 […]