English

English

Credit Utilization Ratio Explained (The 2026 Master Guide)

If you are trying to optimize your personal finances to qualify for a mortgage or unlock premium travel rewards, there is one mathematical formula you must memorize. It dictates 30% of your total FICO credit score, making it the second most important factor behind your payment history.

It is your credit utilization ratio.

While payment history (paying your bills on time) takes years to build, your utilization ratio is highly volatile. It resets every single month. This means it is the easiest metric to accidentally destroy, but it is also the fastest metric you can manipulate to force your credit score upward in under 30 days.

If you are tired of your score flatlining in the high 600s, mastering this single concept is your breakthrough. Here is the ultimate 2026 breakdown of how the credit bureaus calculate your utilization, the dangerous myth of the “30% rule,” and the strategies to optimize your profile.

Table of Contents

- What is a Credit Utilization Ratio? (The Formula)

- Aggregate vs. Per-Card Utilization

- The 30% Myth vs. The 10% Reality

- Why Does the Algorithm Care?

- 3 Strategies to Lower Your Ratio Instantly

- Expert Insight: The 0% Trap

- Frequently Asked Questions (FAQ)

1. What is a Credit Utilization Ratio? (The Formula)

In simple terms, your credit utilization ratio is the percentage of your available credit that you are currently using.

You do not need a degree in finance to figure this out; you just need a calculator. The formula is: Total Credit Card Balances ÷ Total Credit Card Limits = Your Ratio

Let’s look at an example:

- You have one credit card with a $10,000 limit.

- Your current statement balance is $4,000.

- $4,000 ÷ $10,000 = 0.40.

- Your credit utilization ratio is 40%.

Note: This ratio only applies to revolving credit (like credit cards and lines of credit). Installment loans, like your car payment or student loans, are calculated differently and do not factor into this specific percentage.

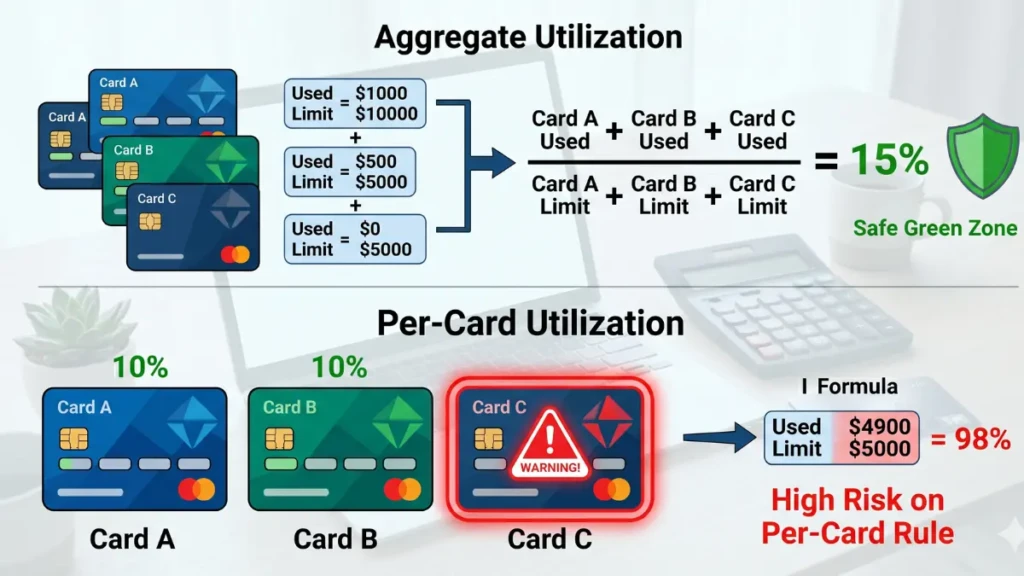

2. Aggregate vs. Per-Card Utilization

One of the biggest mistakes borrowers make in 2026 is misunderstanding how the credit bureaus (Equifax, Experian, TransUnion) view multiple credit cards. The algorithm looks at your utilization in two different ways:

Aggregate Utilization (Your Total Picture): If you have three credit cards, each with a $5,000 limit, your total available credit is $15,000. If your combined balances equal $3,000, your aggregate ratio is an excellent 20%.

Per-Card Utilization (The Hidden Trap): The algorithm also analyzes each card individually. Let’s use the same three cards from above.

- Card A Limit: $5,000 (Balance: $0)

- Card B Limit: $5,000 (Balance: $0)

- Card C Limit: $5,000 (Balance: $3,000)

Even though your aggregate utilization is a safe 20%, Card C is maxed out at 60% utilization. The FICO scoring model will penalize you heavily for having one highly utilized card, dragging your entire score down. You must keep both your aggregate and your per-card utilization low.

3. The 30% Myth vs. The 10% Reality

If you search for advice on credit scores, you will inevitably read: “Keep your credit utilization ratio under 30%.”

In 2026, this is terrible advice if you want an elite credit score. Keeping your utilization at 29% will prevent your score from tanking, but it will not push you into the 750+ range required for the lowest mortgage rates or premium travel credit cards. According to data from FICO, consumers with the highest credit scores (800+) consistently maintain a credit utilization ratio of under 10%, averaging around 7%.

If you want the algorithm to reward you, 10% is the new 30%.

4. Why Does the Algorithm Care?

To understand the rule, you must think like a bank. Credit limits are not “your” money; they are a measure of how much financial rope the bank is willing to give you.

If you earn $60,000 a year and you suddenly max out $25,000 in available credit, the bank’s algorithm assumes you have experienced a cash-flow crisis (like losing your job or facing a massive medical emergency). High utilization signals financial desperation. Low utilization signals that you live well within your means and treat credit as a tool, not a lifeline.

5. 3 Strategies to Lower Your Ratio Instantly

If your ratio is currently sitting at an uncomfortable 45%, here is how you fix it before your next billing cycle:

- The Statement Date Hack: Credit card companies report your balance to the bureaus on your Statement Closing Date, not your due date. Pay your balance down to 5% a few days before the statement closes so the bank reports a tiny balance to the algorithm.

- Request a Limit Increase: If you cannot pay the balance down, ask your bank to increase your limit. If your limit jumps from $5,000 to $10,000 and your balance stays the same, your ratio instantly drops in half. (Ensure the bank does a “soft pull” so it doesn’t trigger a hard inquiry).

- Spread the Spend: If you have multiple cards, do not put all your monthly logistics and travel spending on one card. Spread your purchases across two or three cards to keep your per-card utilization strictly under that 10% threshold.

Expert Insight: The 0% Trap

We consulted with a senior North American credit underwriter about the psychology of perfectionism.

“People assume that if 10% is good, 0% must be perfect. That is false. If you pay your credit card off completely before the statement date and the bank reports a 0% utilization ratio to the bureaus every single month, it looks like you aren’t using the card at all. The FICO algorithm rewards responsible use, not non-use. A 1% or 2% reported ratio will actually yield a higher credit score than a 0% ratio.”

Frequently Asked Questions (FAQ)

Does my credit utilization ratio have a memory?

No. Under the standard FICO 8 scoring model used by most lenders, utilization does not have a “memory.” If your ratio was a terrible 90% last month, but you pay it down to 5% this month, your score will bounce back entirely as soon as the new balance is reported. Note: Newer, less common models like FICO 10T do look at trended data, but FICO 8 remains the industry standard in 2026.

Is a good credit utilization ratio enough to get approved for a mortgage?

No. While it is incredibly important, mortgage lenders look at your entire profile. They heavily weigh your Debt-to-Income (DTI) ratio, your payment history, and your employment stability. However, lowering your utilization is the fastest way to boost your score to secure a lower interest rate.

What happens if I go over my credit limit?

Going over your credit limit means your utilization ratio has exceeded 100%. This is disastrous for your credit score. In addition to severe algorithmic penalties, your bank will likely charge you “over-limit” fees and may even trigger a penalty APR, drastically increasing your interest rate.

Should I close a credit card I no longer use?

Closing an old credit card reduces your total available credit. If you carry balances on other cards, this move will instantly cause your aggregate credit utilization ratio to spike. Unless the card has a high annual fee that you can no longer justify, it is mathematically safer to keep it open and put a small recurring charge on it.

Master the Math, Master the System

Your credit score is not a reflection of your personal worth; it is simply a reflection of how well you play the algorithm’s game. By keeping your credit utilization ratio aggressively low, ideally under 10%, you signal absolute financial stability to North American lenders. Audit your limits today, employ the statement date hack, and watch your score surge.

Ready to optimize the rest of your financial profile? Check out our complete guide on [7 Mistakes That Destroy Your Credit Score (And How to Stop)].