English

English

Amex vs Visa vs Mastercard: The 2026 Network Showdown

When you tap your phone or swipe your plastic at a checkout terminal, the transaction takes less than two seconds. But in the background, a massive digital infrastructure is battling for a fraction of a cent.

If you are a business owner managing corporate ad spend, or a traveler optimizing global logistics, the logo on the bottom right of your credit card dictates where you can spend, how much you are charged in hidden fees, and who you call when a transaction fails.

The debate of Amex vs Visa (and Mastercard) is fundamentally misunderstood. Most people think they are comparing apples to apples. They aren’t. You are actually comparing a software toll-road (Visa/Mastercard) to an entire closed ecosystem (Amex). Furthermore, recent legal settlements in 2026 have completely rewritten the rules on how merchants can treat your premium travel cards.

Here is the deep-dive analytical comparison of Amex vs Visa vs Mastercard, and how to structure your wallet for maximum global acceptance.

Table of Contents

- The Core Difference: Open Loop vs. Closed Loop

- Visa & Mastercard: The Global “Toll Roads”

- American Express: The Premium Ecosystem

- The 2026 Settlement Shockwave

- Global Acceptance: The Reality Check

- Strategic Playbook: The Two-Network System

- Frequently Asked Questions (FAQ)

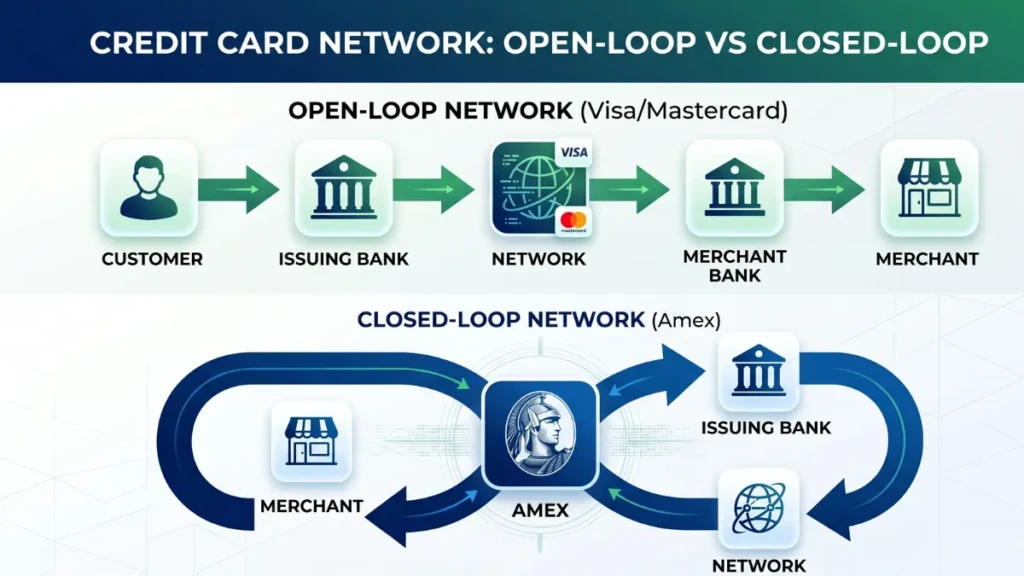

1. The Core Difference: Open Loop vs. Closed Loop

To understand the difference between Visa and Amex, you must understand the difference between a “network” and an “issuer.”

- The Network: The technology pipeline that securely transmits the transaction data between the merchant and the bank.

- The Issuer: The bank that actually lends you the money and manages your account (e.g., Chase, Capital One, Bank of America).

Visa and Mastercard are “Open-Loop” networks. They do not issue credit cards. They do not lend money. They simply build the digital toll road. If you have a Chase Visa card, Chase is lending you the money, but the transaction travels on Visa’s road.

American Express is a “Closed-Loop” network. Amex builds the toll road and they lend you the money. They are both the network and the issuing bank. They control the entire pipeline from start to finish.

2. Visa & Mastercard: The Global “Toll Roads”

When comparing Visa and Mastercard, the truth is that they are virtually identical for the end consumer.

Why they dominate:

- Scale: They are accepted by roughly 100 million merchants worldwide.

- Reliability: You will rarely, if ever, see a “Visa/Mastercard Not Accepted” sign.

- Exchange Rates: Independent studies often show Mastercard offering a microscopically better foreign exchange rate than Visa (usually less than a 0.1% difference), but for daily logistics, it is irrelevant.

Your perks (like travel insurance or cashback) are determined by the issuing bank (like Chase or Capital One), not by Visa or Mastercard.

3. American Express: The Premium Ecosystem

Because Amex is both the bank and the network, they make money on interest, annual fees, and the network swipe fees charged to merchants.

The Amex Advantage:

- Customer Service: If a fraudulent charge appears on a Visa, the merchant blames Visa, and Visa blames Chase. With Amex, there is no finger-pointing. Because they own the whole pipeline, their dispute resolution is widely considered the fastest and most consumer-friendly in the industry.

- Premium Perks: By charging merchants slightly higher swipe fees, Amex funds elite luxury benefits like the Centurion Lounge network and massive multiplier rewards for business spenders.

4. The 2026 Settlement Shockwave

In late 2025 and early 2026, the payments landscape shifted dramatically. Visa and Mastercard reached a historic $38 billion settlement with U.S. merchants regarding swipe fees (interchange fees).

What this means for you: Merchants now have the legal flexibility to surcharge or even reject specific premium cards. If you carry a Visa Infinite (like the Chase Sapphire Reserve) or a World Elite Mastercard, a merchant can legally say, “We accept standard Visa, but we charge a 2% fee if you use a premium rewards Visa.”

This makes the Amex vs Visa vs Mastercard debate highly volatile this year. While Amex was traditionally known as the card merchants hated due to high fees, the new settlement rules mean premium Visa and Mastercard users might start seeing unexpected surcharges at checkout too.

5. Global Acceptance: The Reality Check

In the United States: The acceptance gap has essentially closed. In the US, 99% of merchants that accept credit cards now accept American Express.

International Travel: This is where Amex struggles. In Europe, Asia, and Latin America, merchant fees are heavily regulated. Because Amex relies on higher swipe fees to fund its premium ecosystem, many international merchants simply refuse to accept it. If you are traveling abroad, a Visa or Mastercard with no foreign transaction fees is mandatory.

6. Strategic Playbook: The Two-Network System

No single network is perfect for every scenario. To optimize your cash flow and ensure you are never stranded at a checkout counter, employ the Two-Network Wallet strategy:

- The Premium Workhorse (Amex): Use an American Express card (like the Amex Gold or Business Platinum) for high-multiplier domestic spending, corporate ad spend, and booking flights directly to maximize your point accumulation.

- The Global Backup (Visa or Mastercard): Carry a no-foreign-transaction-fee Visa or Mastercard (like the Capital One Venture X) for international travel, small mom-and-pop shops, and as a fallback if a merchant attempts to apply a new 2026 Visa surcharge.

Frequently Asked Questions (FAQ)

Which is better, Visa or Mastercard?

For the consumer, there is no functional difference. Both networks offer identical global acceptance and security protocols. Your decision should be based entirely on the issuing bank (e.g., choosing a Capital One Mastercard over a Chase Visa because you prefer Capital One’s reward structure).

Why do some places not accept American Express?

American Express typically charges merchants a slightly higher interchange fee (swipe fee) than standard Visa or Mastercard networks. Small businesses operating on razor-thin profit margins often reject Amex to avoid paying those higher transaction costs.

Can I use Amex in Europe?

You can use Amex in Europe at major international hotel chains, large airports, and high-end retail stores. However, if you step out of tourist hubs into local cafes, train stations, or independent restaurants, Amex acceptance drops significantly. You must carry a Visa or Mastercard backup.

Does Discover network work internationally?

Discover is a U.S.-centric network. While it has partnerships with international networks (like UnionPay in China and JCB in Japan), its general acceptance across Europe and South America is incredibly low. It is not recommended as a primary international travel card.

Optimize Your Payment Logistics

Understanding the mechanics of Amex vs Visa allows you to navigate the financial system rather than just reacting to it. By anticipating the 2026 merchant surcharges and carrying a diversified network wallet, you ensure your transactions never fail and your rewards continue to compound.

Looking to optimize the rest of your financial systems? Check out our deep dive on [Venture X vs Sapphire Preferred: Which Is Better in 2026?] to align your business cash flow with your credit strategy.

Best Everyday Credit Card 2026: Maximize Your Daily Spend

15th Apr 2026[…] Amex vs Visa vs Mastercard: The 2026 Network Showdown […]