English

English

How to Avoid Credit Card Interest Completely in 2026

If you are treating your credit card like a high-interest loan, you are bleeding cash. The credit card industry generated billions of dollars in interest revenue last year, and they did it by relying on a simple fact: most consumers do not understand how the system is actually engineered.

In the 2026 financial landscape, where Average Percentage Rates (APRs) frequently hover between 24% and 29%, paying interest is a tax on a lack of strategy. A credit card is supposed to be a cash flow tool that earns you free rewards and protects your money, not a financial anchor.

You do not need to cut up your cards to stop paying the bank. You simply need to understand the mechanics of the billing cycle. If you want to know how to avoid credit card interest completely, forever, here is the exact, zero-fluff system to execute today.

Table of Contents

- The Core Mechanic: The Grace Period System

- The Trap: Statement Balance vs. Current Balance

- The “Trailing Interest” Death Spiral

- The Exceptions: Cash Advances

- The 0% APR Escape Hatch (For Existing Debt)

- Frequently Asked Questions (FAQ)

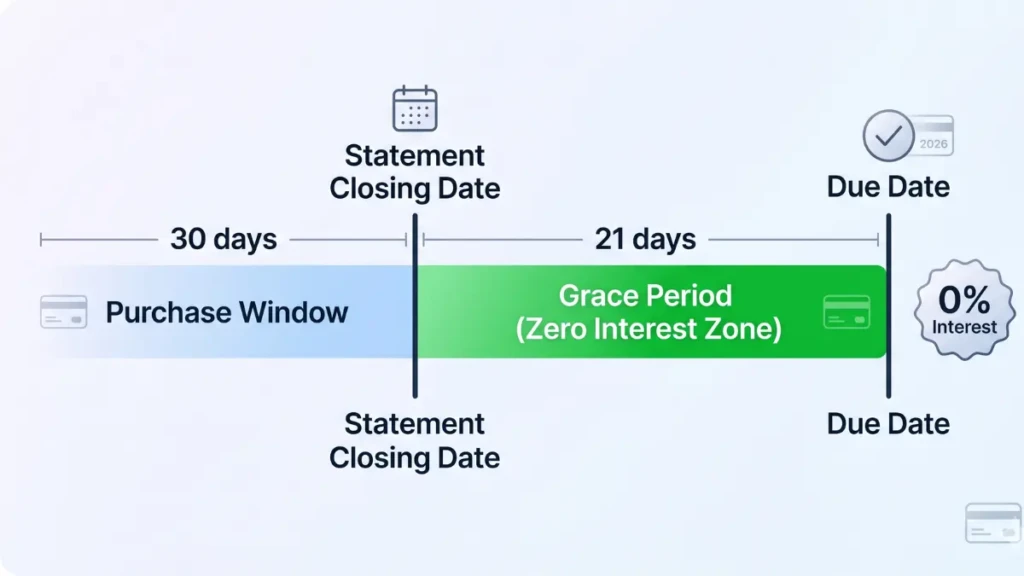

1. The Core Mechanic: The Grace Period System

To avoid paying interest, you must master the “Grace Period.” This is the legal window of time your bank gives you to pay for your purchases before they start charging you extra.

How the Timeline Works:

- The Billing Cycle: Your credit card tracks your purchases for roughly 30 days. Let’s say your cycle runs from March 1st to March 31st.

- The Statement Closing Date: On March 31st, the bank tallies up everything you bought and generates your monthly statement.

- The Grace Period: By federal law, the bank must give you at least 21 days from the statement closing date to pay that bill. This means your payment is due around April 21st.

If you pay the bill in full before the April 21st deadline, the bank charges you 0% interest. You essentially borrowed the bank’s money for over a month, earned cashback or travel points on those purchases, and paid absolutely nothing for the privilege.

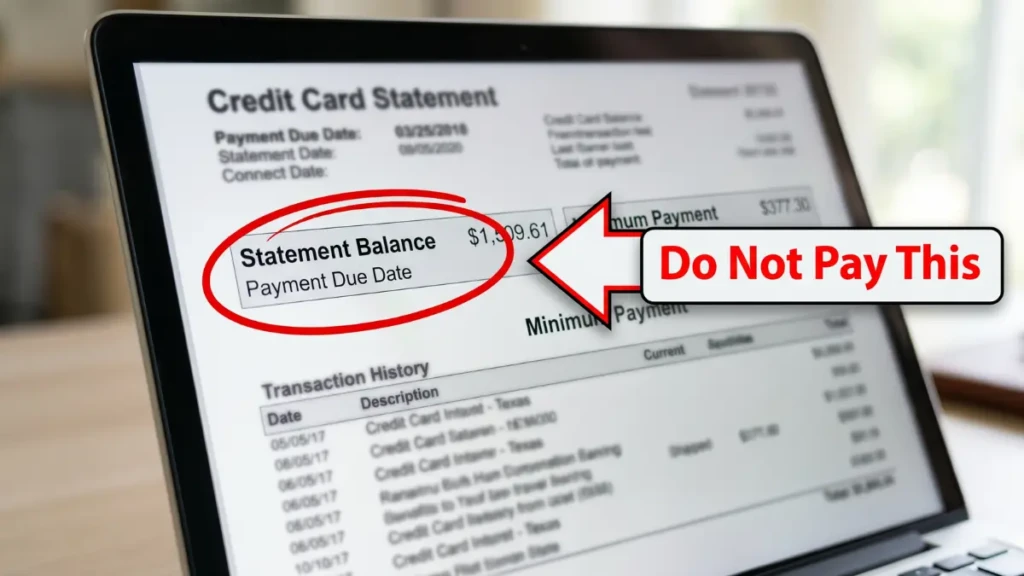

2. The Trap: Statement Balance vs. Current Balance

When you log into your mobile banking app to make your payment, the interface is often designed to confuse you. You will see three numbers: The Minimum Payment, the Statement Balance, and the Current Balance.

- Minimum Payment: This is a trap. If you only pay this, you will be hit with massive interest charges on the remaining balance.

- Current Balance: This includes the purchases from your last billing cycle, plus anything new you bought this week. You do not have to pay this number to avoid interest.

- Statement Balance: This is the exact amount you spent during the 30-day billing cycle that just closed.

The Rule: To completely avoid credit card interest, you must pay the Statement Balance in Full every single month. Set your bank’s auto-pay feature specifically to “Statement Balance.”

3. The “Trailing Interest” Death Spiral

What happens if your statement balance is $1,000, but you only pay $990? You might think you will only pay a few cents of interest on that leftover $10.

You are wrong. The moment you carry a balance into the next month, you instantly lose your Grace Period. This triggers a phenomenon called “Trailing Interest.” Not only will you be charged interest on that leftover $10, but the bank will now start charging you interest on every single new purchase you make from the very day you swipe the card. There is no more 21-day safety net.

To restore your grace period and stop the bleeding, you typically have to pay your statement balance in full for two consecutive billing cycles.

4. The Exceptions: Cash Advances

The Grace Period only applies to standard retail purchases (buying groceries, paying for flights, shopping online). There is a massive exception to the rule that catches many beginners off guard.

Cash Advances: If you take your credit card to an ATM and withdraw physical cash, there is no grace period. Interest begins compounding the exact millisecond the cash leaves the machine. Furthermore, cash advances usually carry a significantly higher APR (often 29.99%) than standard purchases and include an upfront transaction fee. A credit card is for swiping, not withdrawing. Never use it at an ATM.

5. The 0% APR Escape Hatch (For Existing Debt)

The strategies above work perfectly if you currently have a $0 balance. But what if you are already trapped in debt and getting hammered by $200 a month in interest charges?

You need to execute a Balance Transfer.

In 2026, many banks offer 0% Intro APR credit cards. You can transfer your existing high-interest debt onto one of these new cards. The bank will typically charge a one-time transfer fee of 3% to 5%, but they will give you 12 to 21 months of 0% interest to pay off the principal balance.

This freezes the math. Every dollar you pay goes directly toward eliminating your debt, rather than lining the bank’s pockets.

Frequently Asked Questions (FAQ)

Does leaving a small balance on my card help my credit score?

No. This is the most pervasive and destructive myth in personal finance. Leaving a balance on your card does not improve your credit score; it only subjects you to high interest charges. The credit bureaus reward you for having a low “credit utilization ratio,” but paying your statement balance in full accomplishes this without costing you money.

If I pay my bill the day after it’s due, will I be charged interest?

Yes. Missing the due date by even one day terminates your grace period. You will be charged interest on the entire average daily balance of that billing cycle, and you will likely be hit with a late fee (typically around $8 to $32, depending on the issuer and 2026 regulations).

Do I pay interest if I pay my card off multiple times a month?

No. In fact, making multiple payments a month is an excellent strategy. By paying your balance down every Friday, for example, you keep your reported credit utilization ratio extremely low, which boosts your credit score, and you guarantee that you will never carry a balance past the due date.

What happens if I overpay my credit card?

If you accidentally pay more than your current balance, your account will show a negative balance (e.g., -$50). The bank owes you money. There are no penalties or interest charges for this. The $50 credit will simply be applied to your next round of purchases.

Command Your Cash Flow

Learning how to avoid credit card interest is not about financial starvation; it is about system optimization. By treating your credit card like a secure debit card, utilizing auto-pay for the full statement balance, and protecting your grace period at all costs, you turn a liability into a high-ROI asset. Stop paying the bank for access to your own money.

If you want to know how this strategy impacts your FICO score, read our deep dive on [Best Everyday Credit Card 2026: Maximize Your Daily Spend].