English

English

6 Hidden Credit Card Fees You Must Know (2026 Guide)

The credit card industry is a multi-billion dollar machine, and it does not make its primary profit from the people who pay their bills on time. It makes its money by exploiting the fine print.

While annual fees are printed in bold letters on the marketing brochures, the real wealth-drain happens in the background. The average consumer loses hundreds of dollars a year to hidden credit card fees simply because they do not know how to read a “Schumer Box“—the legally mandated table of fees buried in the terms and conditions.

In the 2026 financial landscape, banks have grown incredibly sophisticated at disguising these charges. Whether you are traveling abroad, trying to pay down debt, or just withdrawing cash, you are walking through a financial minefield.

Here are the six most expensive hidden credit card fees you must know, and the exact strategies to avoid them completely.

Table of Contents

- The Cash Advance Trap (The Worst Transaction Possible)

- The “Free” Balance Transfer Fee

- Dynamic Currency Conversion (DCC) Scams

- The 2026 Late Fee Reality

- Foreign Transaction Surcharges

- Subprime “Junk” Fees (Maintenance & Inactivity)

- Expert Insight: Reading the Schumer Box

- Frequently Asked Questions (FAQ)

1. The Cash Advance Trap (The Worst Transaction Possible)

If you take your credit card to an ATM to withdraw physical cash, you have just triggered the most punitive fee structure in the entire banking system. This is known as a Cash Advance.

- The Hidden Fee: The bank will immediately hit you with an upfront transaction fee, typically 5% of the total amount withdrawn (or a flat $10, whichever is greater).

- The Hidden Interest: Unlike normal retail purchases, cash advances have no grace period. The moment the cash leaves the ATM, the bank begins charging you interest compounding daily. Furthermore, the Cash Advance APR is usually significantly higher than your normal purchase APR (often sitting at a brutal 29.99%).

The Fix: Never put a credit card into an ATM. If you need cash, use a debit card.

2. The “Free” Balance Transfer Fee

Banks constantly mail out shiny offers for “0% APR for 18 Months!” to encourage you to transfer your high-interest debt over to their card. While 0% interest sounds like a financial lifeline, it is never free.

- The Hidden Fee: Buried in the fine print is a Balance Transfer Fee, which is almost universally 3% to 5% of the amount transferred.

- The Math: If you transfer $10,000 to a 0% APR card, the bank will immediately tack a $500 fee onto your new balance. You now owe $10,500.

The Fix: A balance transfer is still mathematically smart if it saves you $2,000 in interest over the year, but you must factor that 3-5% upfront fee into your debt-payoff calculations.

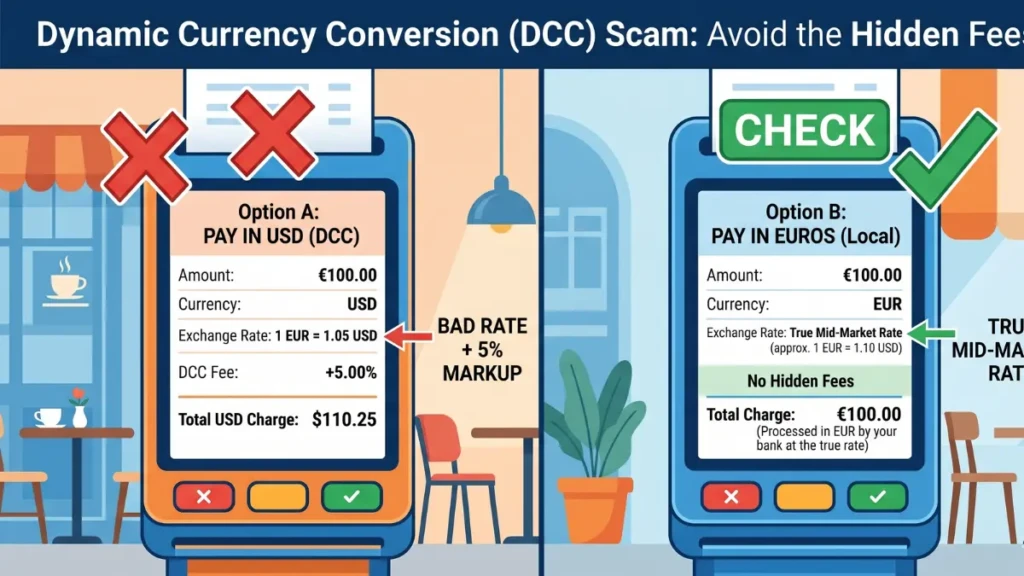

3. Dynamic Currency Conversion (DCC) Scams

When you travel internationally, many payment terminals at cafes or hotels will recognize your foreign card and ask a seemingly helpful question: “Would you like to pay in USD or the local currency?”

- The Hidden Fee: This is called Dynamic Currency Conversion (DCC). If you choose USD, the merchant gets to choose the exchange rate. They will routinely apply a terrible exchange rate that is 5% to 7% worse than the actual mid-market rate. It is a legal tourist trap.

The Fix: Always, without exception, press the button to pay in the local currency. Let your bank do the conversion on the back end, which will be infinitely closer to the true exchange rate.

4. The 2026 Late Fee Reality

If you have been reading outdated financial news, you might think late fees were capped at $8 by the Consumer Financial Protection Bureau (CFPB).

- The Hidden Reality: That 2024 rule was heavily litigated and ultimately vacated by federal courts in 2025. In 2026, credit card late fees have returned to their punitive maximums. Missing your payment by a single day will trigger a late fee of $30 to $41.

- The Trailing Damage: In addition to the fee, you lose your interest grace period, meaning you will start paying interest on all new purchases immediately.

The Fix: Set your bank app to “Auto-Pay: Minimum Balance” so human error never costs you $40 again.

5. Foreign Transaction Surcharges

If you do not have a dedicated travel credit card, using your standard cashback card abroad is a mathematical disaster.

- The Hidden Fee: Most basic credit cards charge a 3% Foreign Transaction Fee on every purchase processed outside of your home country. This completely wipes out any 1% or 2% cashback you might be earning and makes your vacation 3% more expensive across the board.

The Fix: If you plan to travel or buy software from international vendors online, you must carry a dedicated “No Forex Fee” card like the Capital One Venture X or the Chase Sapphire Preferred.

6. Subprime “Junk” Fees (Maintenance & Inactivity)

If you are rebuilding bad credit and are forced to use a subprime “credit-builder” card (from predatory lenders, not reputable secured cards), you will be hammered by junk fees.

- The Hidden Fees: These cards often charge “Monthly Maintenance Fees” ($8 to $12 a month just to keep the account open), “Processing Fees” to pay your bill, and even “Inactivity Fees” if you don’t swipe the card for a few months.

The Fix: Avoid predatory subprime unsecured cards. Instead, use a reputable Secured Credit Card (like Discover it® Secured) which charges absolutely zero junk fees.

Expert Insight: Reading the Schumer Box

We spoke with a consumer rights advocate about how to avoid being blindsided.

“Before you apply for any credit card, scroll down to the link that says ‘Rates and Disclosures.’ This opens the Schumer Box, a federally mandated, standardized chart that lists every fee the card can legally charge you. Look specifically at the ‘Penalty APR’ section. Some cards state that if you miss a single payment, your interest rate jumps to 29.99% permanently. If you don’t read the box, you are agreeing to rules you don’t understand.”

Frequently Asked Questions (FAQ)

Can I get a hidden fee refunded?

Yes, but usually only once. If you are hit with a late fee or an accidental cash advance fee, you can call customer service and ask for a “Goodwill Waiver.” If you are a polite, long-standing customer, banks will often waive the fee as a one-time courtesy.

Does carrying a balance avoid fees?

No. This is a massive myth. Carrying a balance does not “feed” the bank in a way that waives other fees; it simply subjects you to massive interest charges. The best way to avoid fees is to pay your statement balance in full every month.

What is an over-limit fee?

In the past, if you tried to buy something that exceeded your credit limit, the bank would approve it but charge you a $35 “Over-Limit Fee.” Today, thanks to the CARD Act, banks must decline the transaction unless you explicitly “opt-in” to allowing over-limit approvals. Never opt-in.

Are annual fees considered hidden fees?

No. Annual fees are highly visible and heavily marketed as the “cost of entry” for premium cards. Hidden fees are transactional charges that rely on consumer ignorance (like DCC or Cash Advances).

Audit Your Wallet

The banking system relies on the fact that you will not read the fine print. By memorizing these six hidden credit card fees, you build an impenetrable shield around your personal cash flow. Never withdraw cash, always pay in local currency abroad, and automate your minimum payments. Keep your money where it belongs—in your own checking account.

To ensure you are using the right strategies to avoid debt altogether, read our masterclass on [How to Use Credit Cards Smartly in 2026 (Zero Debt, Max Rewards))].