English

English

Best Credit Cards for Beginners in 2026 (USA & Canada)

Starting your financial life from zero can feel like trying to open a door that’s been locked from the inside. You need a credit score to get an apartment, a car loan, or even a premium cell phone plan—but to get that score, you need a credit card.

In 2026, the “Credit Catch-22” is still alive and well. However, banks have become significantly more sophisticated at using “alternative data” (like your history of paying rent or utility bills) to approve your first credit card. Whether you are a student, a newcomer to North America, or simply someone who has avoided debt until now, there is a strategic path to build credit from scratch without falling into a high-interest trap.

If you are looking for the best credit card for beginners, you need a tool that balances high approval odds with actual rewards. Here is the definitive 2026 guide to the top starter cards in the USA and Canada.

Table of Contents

- Interactive Tool: The Beginner Card Finder

- The Secured vs. Unsecured Decision

- Top Starter Cards in the USA

- Top Starter Cards in Canada

- The 6-Month Blueprint to a 700+ Score

- Expert Insight: The 10% Utilization Secret

- Frequently Asked Questions (FAQ)

Interactive Tool: The Beginner Card Finder

Before you apply and risk a “hard pull” on your non-existent credit report, use this tool to determine which category of card you should target based on your current status.Show me the visualization

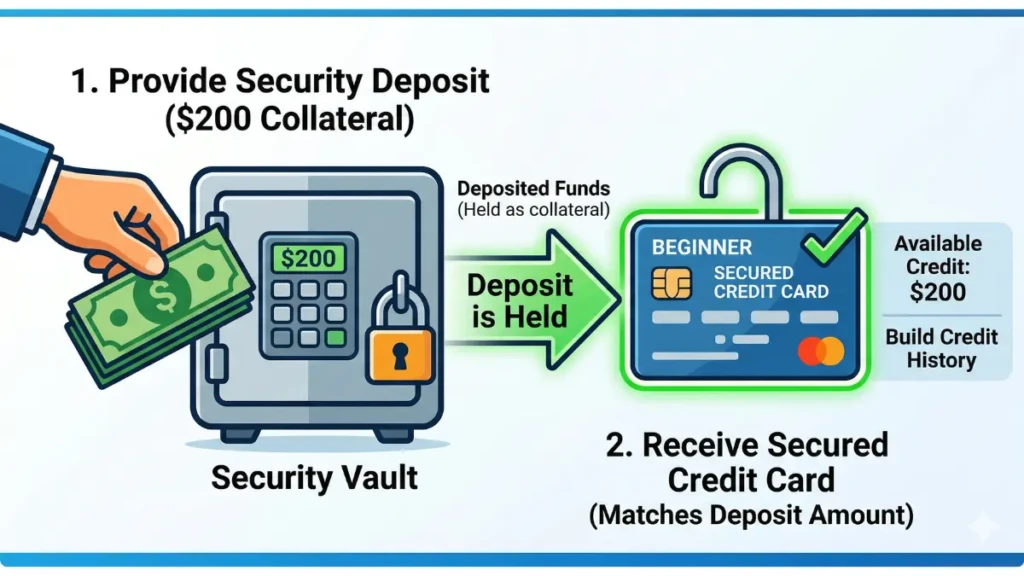

The Secured vs. Unsecured Decision

- Secured Cards: You provide a deposit (e.g., $200) which becomes your credit limit. This acts as “training wheels” for the bank. In 2026, the best secured cards automatically “graduate” to regular cards after 6–8 months of on-time payments, returning your deposit.

- Unsecured Cards: No deposit required. These are harder to get for total beginners but often offer better rewards. If you have a steady income or are a student, you should always try for an unsecured card first.

Top Starter Cards in the USA

- Discover it® Student Cash Back: Consistently the best first credit card for students. It offers 5% cash back on rotating categories and a “Cashback Match” at the end of your first year.

- Capital One Quicksilver Student Cash Rewards: Perfect for those who want simplicity. You get a flat 1.5% cash back on every purchase with no rotating categories to track.

- Discover it® Secured: If you’ve been rejected elsewhere, this is your gold standard. Unlike most secured cards, it actually pays you rewards (2% at gas stations and restaurants).

Top Starter Cards in Canada

- Neo Financial Credit: A disruptor in the Canadian market. It has an incredibly high approval rate for beginners and offers an average of 5% cash back at thousands of partners with no annual fee.

- BMO CashBack® Mastercard®: The best traditional bank option for students. It offers 3% cash back on groceries—the highest in its class for a no-fee beginner card.

- American Express (via Nova Credit): If you are moving to Canada from another country (like India, Australia, or the UK), Amex can use your foreign credit history to approve you for a Canadian card instantly.

The 6-Month Blueprint to a 700+ Score

Getting the card is only 20% of the battle. To build credit from scratch, you must follow the “Beginner’s Rule of Three”:

- The Small Charge: Put one small, recurring subscription (like Spotify or Netflix) on the card.

- The Auto-Pay: Set your card to “Auto-Pay Full Statement Balance.” Never carry a balance or pay interest.

- The Drawer Strategy: After setting up auto-pay, put the physical card in a drawer. Do not use it for daily spending until you’ve mastered the habit of on-time payments.

Expert Insight: The 10% Utilization Secret

We spoke with Sarah Jenkins, a credit consultant for young professionals, about the biggest mistake beginners make.

“Most beginners think that as long as they pay their bill on time, they are fine. But if your credit limit is $300 and you spend $290, your ‘credit utilization’ is 96%. Even if you pay it off in full, the bank reports that high usage to the bureaus, which can actually lower your score. To see your score skyrocket, never let your ‘statement balance’ exceed 10% of your limit ($30 on a $300 card).”

Frequently Asked Questions (FAQ)

How long does it take to get a credit score?

It typically takes six months of activity on your first card before a FICO or TransUnion score can be generated. Before that 6-month mark, your credit report will simply show as “Thin File.”

Should I get a card from my current bank?

Yes. Your “internal score” with your current bank (where you have a checking or savings account) is often higher than your external credit score. They can see your cash flow, making them much more likely to approve your first card.

Does checking my own score hurt it?

No. Checking your own score via apps like Credit Karma (Canada/USA) or your bank’s portal is a “soft pull” and has zero impact on your score.

Ready to Start Building?

Your first credit card is the most important financial tool you will ever own. By choosing a card with no annual fee and focusing on the 10% utilization rule, you can move from “no credit” to a “prime” score in less than a year.

Once you’ve mastered your starter card, you’ll be ready for the big leagues. Read our breakdown on the [Best Credit Cards in 2026: Cashback, Travel & No Annual Fee Options] to plan your next upgrade.

Related Post:

Building Credit from Scratch: A Step-by-Step Guide for New Immigrants in Canada and the USA

Best No Annual Fee Cashback Cards: The 2026 Strategy Guide

13th Apr 2026[…] Best Credit Cards for Beginners in 2026 (USA & Canada) […]