English

English

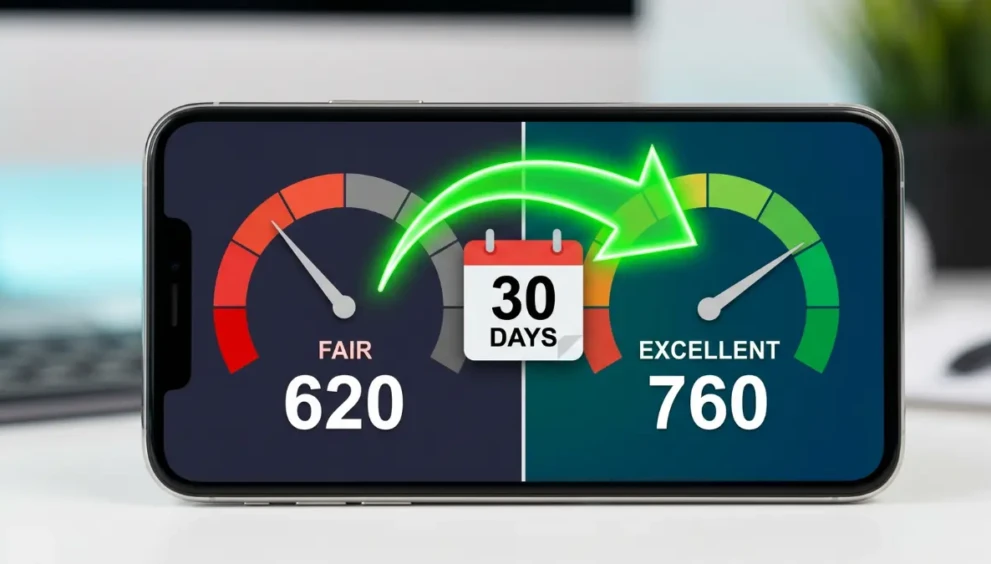

How to Improve Credit Score Fast in 30 Days (2026 Guide)

If you are trying to secure a mortgage, lease a car, or unlock business capital in the United States or Canada, your three-digit credit score dictates your financial reality. When that score is sitting in the low 600s, you don’t have time for traditional advice like “just keep paying your bills on time for the next three years.” You need immediate results.

The modern FICO algorithm is a highly predictable mathematical machine. It has specific levers you can pull to force it to recalculate your risk profile. If you know how the credit bureaus (Experian, Equifax, TransUnion) process data, you can engineer a massive point jump in a matter of weeks.

If you need to know how to improve credit score fast, this is not a theoretical guide. This is a strict, 30-day operational timeline designed to manipulate the system, lower your risk profile, and fix bad credit fast.

Table of Contents

- Days 1-7: The “Statement Date” Utilization Hack

- Days 8-14: The Authorized User Shortcut

- Days 15-21: Strategic Credit Limit Increases

- Days 22-30: Instant Alternative Data Injections

- Expert Insight: The “Pay-For-Delete” Negotiation

- Frequently Asked Questions (FAQ)

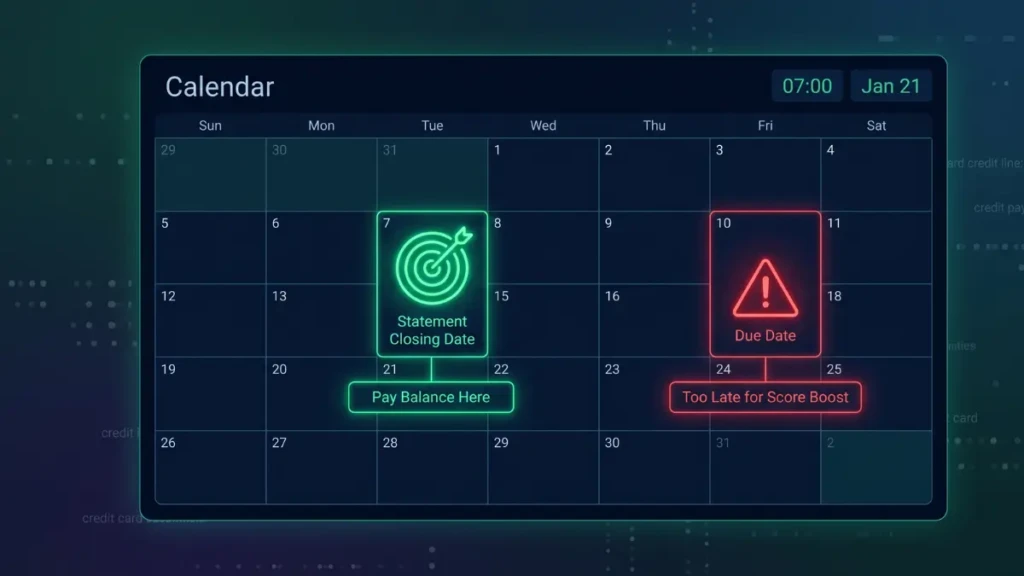

1. Days 1-7: The “Statement Date” Utilization Hack

Your Credit Utilization Ratio (the amount of debt you carry versus your total available credit limit) dictates 30% of your entire FICO score. It is highly volatile, meaning it has no memory. If you fix it today, your score skyrockets the moment it is reported.

This is the absolute fastest way to increase credit score quickly.

The Execution:

- Do not pay your credit card on the “Due Date.” Pay it 3 days before the “Statement Closing Date.”

- The Statement Closing Date is the exact day the bank reports your balance to the credit bureaus. If you pay your balance down to 5% before this date, the algorithm thinks you are barely using your card, signaling elite financial stability.

- The ROI: Dropping your reported utilization from 80% to under 10% can trigger a 40 to 60-point score jump in a matter of days.

2. Days 8-14: The Authorized User Shortcut

If your credit file is “thin” (meaning you don’t have a long history of borrowing), you can legally hijack someone else’s excellent credit history through a process called “Piggybacking.”

The Execution:

- Find a highly trusted family member or partner who has a credit card with three specific traits: a high credit limit, a perfect payment history, and an old account age (5+ years).

- Ask them to add you as an Authorized User on that specific card. (They do not actually have to give you the physical card; they just need to add your name to the account).

- The ROI: Within 15 to 30 days, the entire flawless history of that specific credit card will copy and paste onto your personal credit report, instantly thickening your file and spiking your score.

3. Days 15-21: Strategic Credit Limit Increases

If you do not have the liquid cash to pay down your credit card balances right now, you can still improve your utilization ratio from the other side of the equation.

The Execution:

- Log into your banking apps and request a Credit Limit Increase (CLI) on all your current cards.

- Crucial Step: You must ensure the bank only does a “Soft Pull” (which does not affect your score) rather than a “Hard Pull.” Most major issuers in 2026 allow soft-pull CLIs directly in their mobile apps.

- The ROI: If your current balance is $2,500 on a $5,000 limit card, your utilization is a damaging 50%. If the bank raises your limit to $10,000, your utilization instantly drops to an excellent 25% without you paying a single dime.

4. Days 22-30: Instant Alternative Data Injections

If you have a thin file and need to improve credit score fast, you can force the bureaus to recognize the bills you are already paying.

The Execution:

- Connect your primary checking account to services like Experian Boost or Equifax eCredable.

- These free tools scan your bank account for recurring, on-time payments for utilities, mobile phone bills, and streaming services (like Netflix or Hulu) and inject them into your credit file as positive payment history.

- The ROI: This process is nearly instantaneous. While it won’t fix major delinquencies, the average user sees a fast 10 to 15-point increase the moment the data connects.

Expert Insight: The “Pay-For-Delete” Negotiation

We consulted a North American credit underwriting specialist about the fastest way to handle existing collections accounts.

“If you have a $500 medical bill or old utility bill sitting in collections, simply paying it off will not remove the red flag from your credit report. It will just change the status to ‘Paid Collection,’ which still hurts your score. To fix bad credit fast, you must negotiate a ‘Pay-for-Delete’ agreement. Call the collection agency and offer to pay the debt in full right now, but ONLY if they agree in writing to delete the entire trade line from all three credit bureaus. Once deleted, it is as if the negative mark never existed.”

Frequently Asked Questions (FAQ)

Can paying off a collection drop my credit score?

Strangely, yes. If a collection account is 4 years old, the FICO algorithm has already factored in the damage. If you pay it off today without a “Pay-for-Delete” agreement, it updates the “Date of Last Activity” to today, making the negative mark look brand new to the algorithm, which can temporarily tank your score.

Does checking my own credit score lower it?

No. Checking your own score through a monitoring app or directly through your bank is considered a “Soft Inquiry” and has absolutely zero impact on your score. Only “Hard Inquiries” (when a lender checks your credit because you applied for new debt) will cause a temporary 2 to 5-point drop.

How fast is a “Rapid Rescore”?

If you are currently sitting with a mortgage broker and are 10 points shy of approval, they can execute a formal “Rapid Rescore.” After you pay down a credit card balance, your broker submits the proof directly to the bureaus for a fee. The bureaus manually update your score within 48 to 72 hours, rather than waiting 30 days for the normal reporting cycle.

Master the Algorithm

A bad credit score is not a permanent life sentence; it is simply a reflection of an unoptimized system. By memorizing the reporting dates, executing strategic limit increases, and leveraging authorized user status, you take complete control of the algorithm. Execute this 30-day timeline to improve credit score fast and secure the capital you need to scale your life.

To ensure you don’t make critical errors while rebuilding, read our foundational guide on [Debit vs Credit Card: The Hidden Truth (2026 Guide)].

Best No Annual Fee Credit Cards 2026: The High-ROI Strategy

23rd Apr 2026[…] How to Improve Credit Score Fast in 30 Days (2026 […]

Best No Annual Fee Credit Cards in the USA (2026 Guide)

27th Apr 2026[…] How to Improve Credit Score Fast in 30 […]