English

English

What Happens If You Miss a Credit Card Payment? (2026 Guide)

In a highly optimized financial system, your cash flow should operate on autopilot. But when a manual error occurs and you miss a credit card payment, the psychological panic is usually worse than the actual mathematical reality.

The banking system relies on fear to enforce compliance, but the penalty system is actually a rigid, predictable machine. If you are 24 hours late, your credit score is not ruined. However, if you do not understand the exact timeline of a late payment penalty, a simple administrative mistake can compound into thousands of dollars in hidden interest.

If you just missed your due date and need to assess the damage, stop panicking. Here is the strict, chronological breakdown of exactly what happens when you pay late, the hidden costs the banks don’t advertise, and the tactical steps to eradicate the penalties today.

Table of Contents

- Phase 1: Days 1 to 29 (The Financial Penalty)

- Phase 2: Day 30 (The Algorithmic Cliff)

- Phase 3: Day 60+ (The Penalty APR)

- The Fix: The “Goodwill” Negotiation Strategy

- Expert Insight: Automating Your Defense

- Frequently Asked Questions (FAQ)

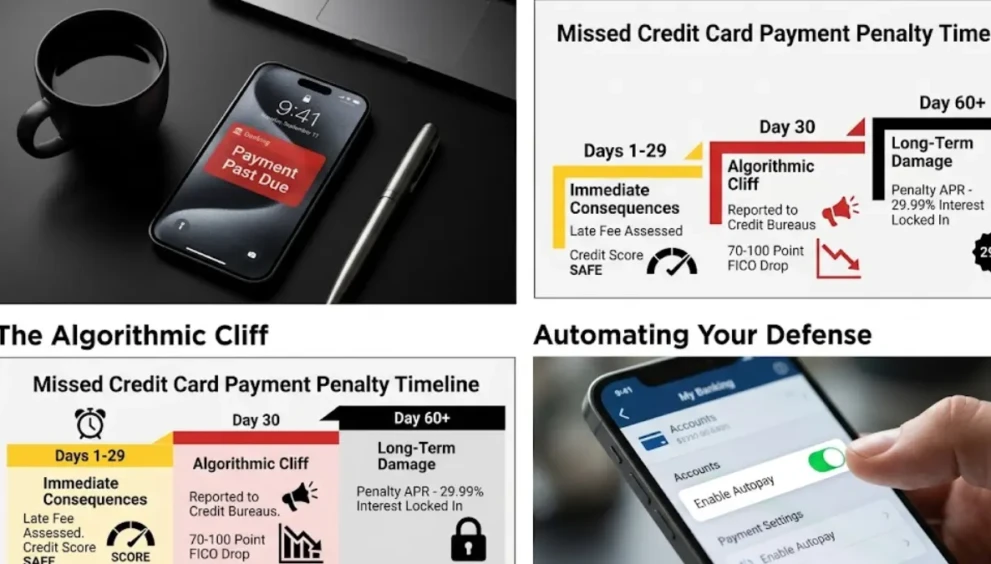

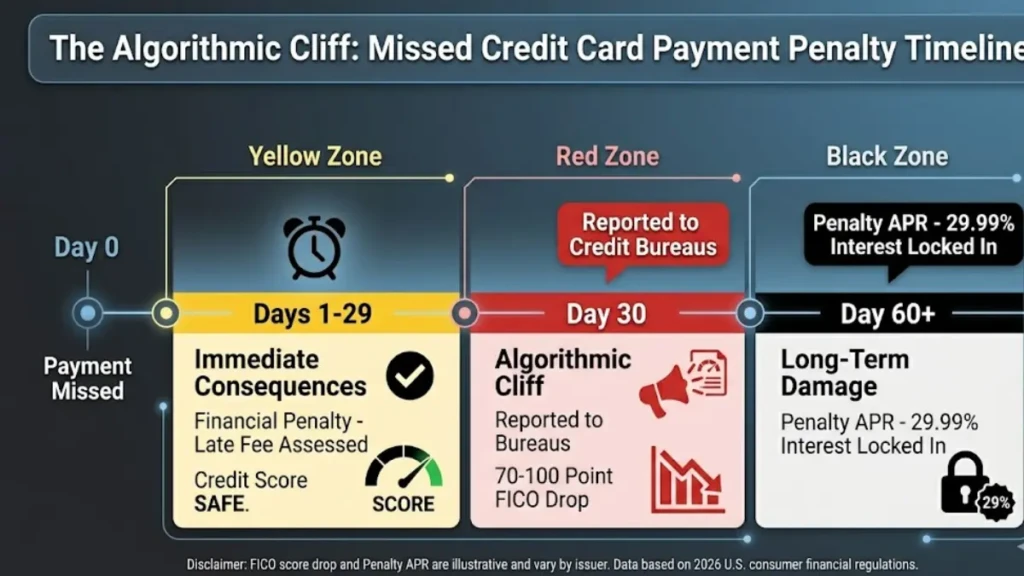

1. Phase 1: Days 1 to 29 (The Financial Penalty)

If you are reading this and you are between 1 and 29 days late, take a deep breath. Your credit score has not been impacted. By federal law, credit card issuers cannot report a late payment to the credit bureaus (Experian, Equifax, TransUnion) until it is a full 30 days past due. However, you will immediately face two distinct financial consequences.

- The Late Payment Penalty: The moment midnight passes on your due date, the bank will automatically assess a late fee. In 2026, this fee typically ranges between $8 and $40, depending on the card and your previous payment history.

- The Loss of the Grace Period: This is the hidden “tax.” When you miss a payment or carry a balance, you instantly forfeit your 21-day interest-free grace period. This means any new purchases you make tomorrow will start accruing daily interest the exact second you swipe the card.

2. Phase 2: Day 30 (The Algorithmic Cliff)

Day 30 is the most critical deadline in personal finance. If your account remains unpaid for a full 30 days past the original due date, the bank automatically triggers a report to the credit bureaus.

- The FICO Damage: Payment history accounts for 35% of your total FICO score. A single 30-day late mark can cause an immediate, devastating drop of 70 to 100 points, depending on how high your score was prior to the incident.

- The Longevity: This negative mark will remain anchored to your credit report for seven years. While the algorithmic impact lessens over time, it will immediately disqualify you from premium auto loans, top-tier travel cards, and optimal mortgage rates for the near future.

3. Phase 3: Day 60+ (The Penalty APR)

If you allow the missed payment to reach 60 days late, the bank shifts from issuing warnings to actively penalizing your capital.

- The Penalty APR: At the 60-day mark, the bank is legally allowed to revoke your standard interest rate (e.g., 18%) and apply the Penalty APR, which is almost universally set at a crippling 29.99%.

- The Snowball Effect: This 29.99% rate applies to your entire existing balance, not just new purchases. Your minimum payments will skyrocket, and the mathematical effort required to escape the debt will double overnight. Furthermore, the bank will likely slash your credit limit, destroying your credit utilization ratio and tanking your score even further.

4. The Fix: The “Goodwill” Negotiation Strategy

If you just realized you are 3 days late, you can fix this in under 10 minutes. Banks do not want to lose a profitable customer over a single administrative error.

The Execution:

- Pay Immediately: Log into your app right now and pay at least the minimum due. Do not wait.

- Call the Retention Line: Call the number on the back of your card. Do not use the automated chatbot.

- The Script: “Hi, I noticed a late fee on my account. I have been a loyal customer with a perfect payment history for [X] years. I made an administrative error with my banking calendar this month, but I just paid the balance in full. As a one-time courtesy, can you please waive this late fee?”

In 95% of cases involving a first-time offense, the representative will click a button, reverse the fee, and restore your account to perfect standing.

Expert Insight: Automating Your Defense

We asked a systemic wealth manager why highly successful professionals still miss payments.

“Missing a payment is rarely a cash flow issue; it is a systems issue. If you rely on your memory to pay five different credit cards on five different dates, you will eventually fail. To permanently eliminate the risk of a late payment penalty, you must build an automated defense. Set every single credit card to ‘Autopay: Minimum Balance.’ Even if you manually log in later to pay the statement in full, that automated minimum acts as an infallible safety net, guaranteeing you will never hit the 30-day credit score cliff.”

Frequently Asked Questions (FAQ)

Will paying a day late ruin my credit score?

No. Credit card companies only report to the credit bureaus when an account is a full 30 days past due. If you pay on day 2 or day 15, you will likely incur a late fee and interest charges, but your FICO score will remain completely untouched.

What happens if I miss a credit card payment but have a 0% APR promo?

This is a massive trap. If you are operating under a 12-month 0% APR promotional period and you miss a credit card payment, read your fine print. Most banks include a clause stating that a single late payment instantly voids the 0% promotion, permanently reverting your account to the standard 20%+ interest rate.

Can I get a 30-day late mark removed from my credit report?

It is difficult, but possible. If the bank has already reported the 30-day late mark to the bureaus, you can write a formal “Goodwill Adjustment Letter” to the bank’s executive offices. Explain the hardship that caused the delay, highlight your years of perfect history, and politely ask them to request a deletion from the bureaus. It is not guaranteed, but high-value customers often succeed.

Command Your Infrastructure

A missed payment is an operational leak, not a permanent disaster. By understanding that you have a 29-day buffer to protect your FICO score, you eliminate the panic. Call the bank, negotiate the fee reversal, and immediately set up your minimum autopay safety net. Stop relying on memory and start relying on systems.

Looking to upgrade your financial toolkit now that your score is safe? Review our master guide on the [Best No-Annual-Fee Credit Cards of April 2026: Ultimate Guide].

Cost of Living USA (2026 Breakdown): What You Actually

27th Apr 2026[…] What Happens If You Miss a Credit Card Payment? (2026 […]