English

English

How to Build Credit from Scratch: The 2026 Fast-Track Guide

If you have never taken out a loan or opened a credit card, you might assume you are in a great financial position. After all, zero debt is a good thing, right?

In the eyes of the North American financial system, the answer is a resounding no. If you are looking at how to build credit from scratch, you are facing a frustrating paradox: banks won’t give you a credit card because you don’t have a credit history, but you can’t build a credit history without a credit card.

Having a “ghost” file—meaning no credit score at all—is often treated the same as having a bad credit score. Without a proven track record, landlords will reject your apartment applications, auto insurance companies will charge you higher premiums, and navigating travel logistics (like putting a hold on a rental car or booking a hotel room) becomes incredibly difficult if you only have a debit card. Furthermore, an invisible credit profile locks you out of the lucrative world of premium travel rewards and cashback points.

Fortunately, the financial landscape in 2026 offers tools specifically designed to solve this exact problem. You do not need to go into debt to prove you are responsible. Here is the step-by-step, fast-track guide to generating an excellent credit score from absolutely nothing.

Table of Contents

- Strategy 1: The “No Credit History” Credit Card (Secured)

- Strategy 2: The Authorized User Hack (Piggybacking)

- Strategy 3: Credit-Builder Loans

- Strategy 4: Alternative Data (Rent & Utilities)

- The 3 Golden Rules of Credit Maintenance

- Expert Insight: The Hard Pull Trap

- Frequently Asked Questions (FAQ)

Strategy 1: The “No Credit History” Credit Card (Secured)

If you have zero credit, applying for a standard, unsecured rewards card will result in an automatic rejection (which actually hurts your future chances). Your first step should be applying for a no credit history credit card, commonly known as a Secured Credit Card.

How it works: You put down a refundable cash deposit—usually between $200 and $500. This deposit acts as your credit limit. If you put down $300, your card will have a $300 limit. You then use the card to make small purchases and pay the bill off every month.

Because the bank holds your cash as collateral, there is zero risk to them, meaning approval is nearly guaranteed regardless of your credit history.

Top 2026 Recommendations:

- Discover it® Secured Credit Cardhttps://www.discover.com/credit-cards/secured-credit-card/: Widely considered the best starter card in the US because it charges no annual fee, actually offers cashback rewards on dining and gas, and automatically reviews your account after 7 months to upgrade you to an unsecured card (and return your deposit).

- Capital One Platinum Secured: Excellent for its low barrier to entry, sometimes allowing you to secure a $200 credit line with a deposit as low as $49, depending on your application.

Strategy 2: The Authorized User Hack (Piggybacking)

If you want to build credit fast without putting down a cash deposit, you can legally “borrow” someone else’s good credit history.

How it works: Ask a trusted family member or partner who has an excellent credit score and a long-standing credit card account to add you as an “Authorized User.”

When they add your name to their account, the entire history of that specific credit card is copied and pasted onto your blank credit report. If they have had the card for five years and never missed a payment, it suddenly looks like you have five years of perfect payment history.

The Golden Rule: You do not even need to possess the physical card or spend their money. They can cut the secondary card in half the moment it arrives in the mail. As long as your name is on the account, you reap the credit-building benefits.

Strategy 3: Credit-Builder Loans

If you do not want the temptation of a plastic card in your wallet, a credit-builder loan is a fantastic, forced-savings method to generate a score.

How it works: Unlike a traditional loan where the bank hands you money upfront, a credit-builder loan works in reverse. You apply for a small loan (e.g., $1,000) through a credit union or a service like Self. The lender approves the loan but places the $1,000 in a locked savings account.

You make fixed monthly payments (e.g., $85 a month) toward the loan. The lender reports these on-time payments to the credit bureaus (Experian, Equifax, TransUnion). Once you have paid off the total amount, the locked savings account is released to you. You built credit, and you built a $1,000 emergency fund simultaneously.

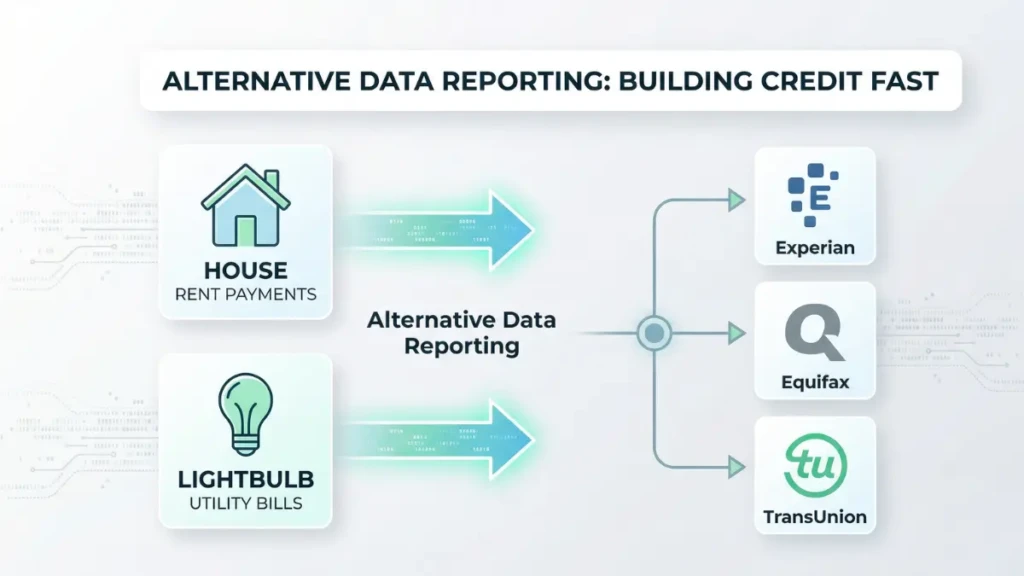

Strategy 4: Alternative Data (Rent & Utilities)

For decades, the biggest financial injustice was that missing a rent payment could ruin your credit, but paying rent on time for ten years did absolutely nothing to build it. In 2026, the system has finally adapted.

You can now use “Alternative Data” to establish your FICO and VantageScore ratings from scratch.

How to report your bills:

- Experian Boost: A free service that connects to your bank account and scans for on-time payments to utility companies, telecom providers, and even streaming services (like Netflix or Hulu), adding them to your Experian credit file.

- Rent Reporting Services: Platforms like Boom, RentTrack, or Bilt Rewards will verify your monthly rent payments and report them to all three major bureaus. Because rent is usually your largest monthly expense, having it show up as an “on-time payment” builds trust with the algorithm incredibly fast.

The 3 Golden Rules of Credit Maintenance

Opening an account is only 10% of the battle. How you manage that account determines whether you build an “average” score of 650 or an “elite” score of 780+.

- Never Miss a Payment (100% On-Time): Payment history makes up 35% of your total credit score. Set up automatic payments for at least the minimum balance immediately. A single payment that is 30 days late will tank a brand-new credit score and stay on your report for seven years.

- Keep Utilization Below 10%: Credit utilization is how much of your available credit you are using. If you have a $500 limit and spend $450, your utilization is 90%—which signals financial panic to the algorithm. To build credit fast, spend $30 on the card (like a single tank of gas or a phone bill), let the statement post, and pay it off.

- Pay in Full, Avoid Interest: You do not need to carry a balance or pay interest to build credit. That is a toxic financial myth. Pay your statement balance in full every single month.

Expert Insight: The Hard Pull Trap

We asked a former credit underwriter what the most common mistake beginners make when trying to escape a “thin” credit file.

“Panic applying. When someone realizes they have no credit, they often go online and apply for five different credit cards in a single weekend, hoping one will say yes. Every application triggers a ‘Hard Inquiry’ on your credit report, which dings your score. If you have no history and suddenly accumulate five hard inquiries, the algorithm flags you as high-risk and desperate for credit. Apply for one secured card. Stop. Wait six months before applying for anything else.”

Frequently Asked Questions (FAQ)

How long does it take to get a credit score from scratch?

It takes a minimum of six months of reported activity to generate a standard FICO credit score. VantageScore algorithms are slightly faster and can sometimes generate a score in one to two months, but most major lenders in North America still rely heavily on the six-month FICO timeline.

Is no credit worse than bad credit?

In many logistical scenarios, yes. Lenders view “bad credit” as a known risk, but they view “no credit” as an unpredictable total unknown. It is often easier to get approved for a subprime loan with a bad score than it is to get approved with a blank file.

Can I build credit with a debit card?

No. Traditional debit cards pull cash directly from your checking account. Because you are not borrowing money, the banks do not report debit card activity to the credit bureaus.

Does checking my own credit score lower it?

No. Checking your own credit score through a banking app or a free service like Credit Karma is considered a “Soft Inquiry” (or soft pull). Soft inquiries do not impact your credit score whatsoever. You should check your score at least once a month to monitor for identity theft.

What is the best way to transition from a secured to an unsecured card?

Use your secured card responsibly for 6 to 8 months by keeping the utilization under 10% and paying in full. Many issuers (like Discover or Capital One) will automatically review your account and upgrade you. If they don’t, you can call customer service and request a “product change” to an unsecured card, which allows you to keep the account history open while getting your deposit back.

Your Financial Passport

Think of your credit score as your financial passport. Without it, you are locked out of the best travel rewards, the cheapest auto loans, and the most desirable apartments. By starting with a secured card, leveraging your monthly rent payments, and keeping your utilization aggressively low, you can transform a blank slate into an elite 750+ credit score in less than a year.

Once your score is established, check out our guide on [I Tried 7 Credit Cards in Canada — Best One Worth Keeping] to start making your credit work for you.

Secured vs Unsecured Credit Cards: Which Is Better in 2026?

13th Apr 2026[…] How to Build Credit from Scratch: The 2026 Fast-Track Guide […]

Best No Annual Fee Cashback Cards: The 2026 Strategy Guide

13th Apr 2026[…] How to Build Credit from Scratch: The 2026 Fast-Track Guide […]

Venture X vs Sapphire Preferred: Which Is Better in 2026?

15th Apr 2026[…] How to Build Credit from Scratch: The 2026 […]