English

English

Secured vs Unsecured Credit Cards: Which Is Better in 2026?

Standing at the entrance of the credit-building world feels like a “Catch-22.” You need a credit card to build a score, but you need a score to get a credit card. This leads almost every beginner to a critical crossroads: secured credit card vs unsecured.

The choice you make today determines how much you’ll pay in fees, how quickly your score will climb, and how soon you can unlock high-tier travel rewards. In 2026, the lines between these two categories are blurring thanks to new technology, but the fundamental mechanics remain the same.

If you are starting from scratch or repairing a damaged history, understanding the math behind these two tools is the only way to avoid leaving money on the table.

Table of Contents

- The Mechanics of the Secured Credit Card

- The Standard: Unsecured Credit Cards Explained

- Side-by-Side Comparison: The 2026 Breakdown

- The 2026 Fintech Shift: AI and Cash-Flow Underwriting

- Which One Should You Choose?

- Expert Insight: The Graduation Strategy

- Frequently Asked Questions (FAQ)

1. The Mechanics of the Secured Credit Card

A secured credit card is effectively a “training wheels” card. It is designed specifically for those whom banks consider high-risk—people with no credit history or a history of missed payments.

How it works:

The defining feature of a secured card is the security deposit. You provide the bank with a refundable deposit (typically $200 to $500), and that deposit becomes your credit limit. If you give them $300, your limit is $300.

Contrary to popular belief, the bank does not spend your deposit to pay for your groceries. You still have to pay your monthly bill just like a normal card. The deposit sits in a locked account as collateral. If you disappear and stop paying your bill, the bank takes your deposit to cover the loss. Because there is zero risk for the bank, approval is almost guaranteed.

2. The Standard: Unsecured Credit Cards Explained

An unsecured credit card is what most people think of as a “normal” credit card. It does not require a deposit. Instead, the bank extends you a line of credit based purely on their trust in your ability to pay them back.

How it works:

The bank looks at your credit score and income. If they like what they see, they give you a limit (e.g., $2,000) that is backed by nothing but your signature.

For beginners, unsecured starter credit cards are the “Gold Standard.” They allow you to keep your cash in your own pocket while earning rewards like 1% or 2% cash back. However, the requirements are higher. If your FICO score is below 650, or if you have a “thin file” (no history at all), getting approved for a traditional unsecured card can be difficult.

3. Side-by-Side Comparison: The 2026 Breakdown

| Feature | Secured Credit Card | Unsecured Credit Card |

| Security Deposit | Required (Refundable) | None |

| Credit Score Needed | 300 – 600 (or None) | 650+ (Usually) |

| Credit Limit | Usually equal to deposit | Based on income and credit |

| Rewards & Perks | Minimal (Becoming more common) | High (Cash back, travel points) |

| Risk of Rejection | Extremely Low | Moderate to High |

4. The 2026 Fintech Shift: AI and Cash-Flow Underwriting

The most significant change in 2026 is how banks judge “trust.” In the past, no credit score meant a mandatory secured card. Today, a new wave of fintech companies (like Chime, Petal, and Fizz) uses cash-flow underwriting.

Instead of just looking at your credit report, they ask to link your primary bank account. Their AI analyzes your income, your spending habits, and your average daily balance. If you show a consistent “green” cash flow, they may approve you for an unsecured starter credit card even if you have a score of zero.

Pro Tip: If you have a steady job and some savings, check for “Pre-Approval” with fintech lenders before tying up your cash in a secured deposit.

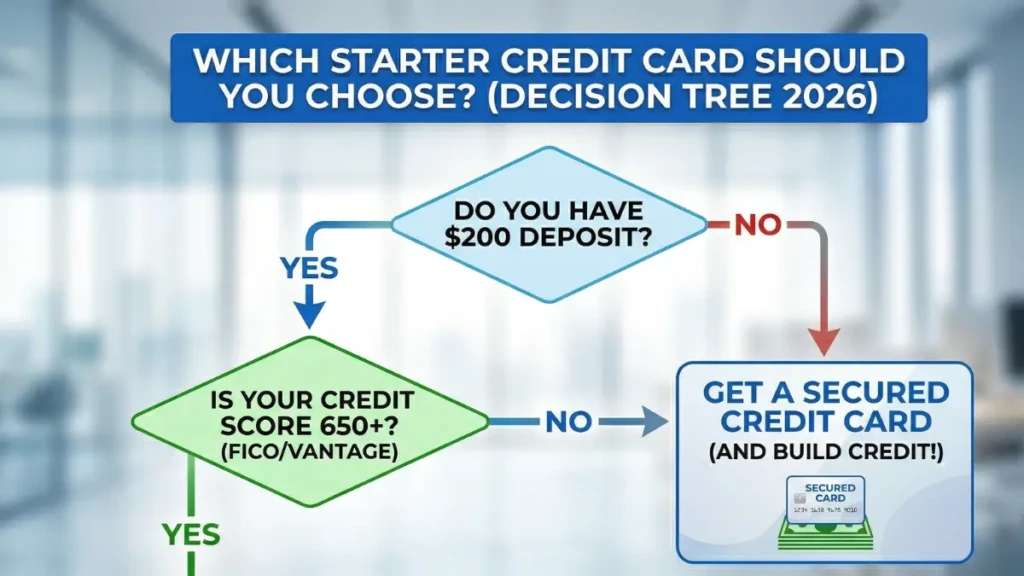

5. Which One Should You Choose?

The decision boils down to your current data:

- Choose a Secured Card if: You have a history of bankruptcy, multiple late payments, or you have been rejected for two or more unsecured cards in the last 90 days. It is the surest way to force your score upward.

- Choose an Unsecured Card if: You have a clean (but empty) file, a steady income, and a score above 650. This keeps your capital free and allows you to start earning rewards immediately.

Expert Insight: The Graduation Strategy

We asked a senior credit analyst about the most efficient path to an 800 score.

“Don’t stay in a secured card longer than you have to. Many beginners forget they have a $500 deposit sitting idle. In 2026, most major issuers like Discover and Capital One have a ‘Graduation’ policy. If you make 7 to 12 on-time payments, they will automatically review your account, return your deposit, and convert the card to a standard unsecured account. Always ask about the graduation timeline before you apply. If a card doesn’t offer a path to graduation, find one that does.”

Frequently Asked Questions (FAQ)

Do I get my security deposit back?

Yes. Your deposit is fully refundable. You get it back either when you close the account in good standing (with a $0 balance) or when the bank “graduates” you to an unsecured card.

Is a secured card better for my credit score than an unsecured one?

No. Both cards report to the three major credit bureaus (Experian, TransUnion, Equifax). As far as the credit score algorithm is concerned, they are identical. The only thing that matters is your payment history and your utilization ratio.

What is the minimum deposit for a secured card?

In 2026, most secured cards require a minimum of $200. Some “partial” secured cards may allow you to open a $200 line with a $49 or $99 deposit if you meet certain income criteria.

Can I use a secured card for travel and hotels?

Yes, but be careful. Hotels and car rental agencies often place a “hold” on your card for incidentals. If your limit is only $300 and the hotel places a $200 hold, you will only have $100 left for spending, which could cause your card to be declined elsewhere.

Step Into Your Financial Future

Whether you choose the safety of a secured card or the rewards of an unsecured one, the goal remains the same: 100% on-time payments. In the 2026 economy, your credit score is your most valuable asset. Pick the tool that fits your current reality, use it responsibly, and watch the doors to premium travel and lower interest rates swing open.

Ready to start your journey? Check out our guide on How to Build Credit from Scratch: The 2026 Fast-Track Guide] to see the exact steps to your first 700 score.

Best Travel Credit Cards 2026: The Ultimate North American Guide

13th Apr 2026[…] Secured vs Unsecured Credit Cards: Which Is Better in 2026? […]