English

English

Best Everyday Credit Card 2026: Maximize Your Daily Spend

While premium travel cards get all the glossy marketing, the reality of personal finance is much less glamorous. You likely book a major flight once or twice a year, but you buy groceries, pump gas, and pay for coffee every single week.

If you are only optimizing for luxury travel, you are missing out on the largest segment of your personal cash flow. The foundational piece of any modern wallet is the everyday credit card—also known as your “daily driver.”

In 2026, the definition of a great daily driver has evolved. With the cost of groceries and dining taking up a larger percentage of the average budget, a card that earns 1% back is no longer acceptable. You need a card that actively fights inflation by returning 2%, 3%, or even 4% on your most common expenses.

Whether you want the “set it and forget it” simplicity of a flat-rate card, or a highly optimized category multiplier, here is the analytical breakdown of the best credit cards for everyday spending this year.

Table of Contents

- The Minimalist: Best Flat-Rate Catch-All Cards

- The Foodie: Best for Groceries and Dining

- The Commuter: Best for Gas and Transit

- The 2026 Trend: Mobile Wallet Multipliers

- Strategic Playbook: The “Bifurcated” Wallet

- Expert Insight: Beware the “Caps”

- Frequently Asked Questions (FAQ)

1. The Minimalist: Best Flat-Rate Catch-All Cards

If you hate tracking rotating categories and refuse to carry more than one card, you need a flat-rate everyday credit card. The golden standard in 2026 is 2% cash back on everything.

Citi Double Cash® Card

- The Reward: 2% cash back (1% when you buy, 1% when you pay your bill).

- Why it Wins: It builds great financial habits by rewarding you for paying your statement. It is the ultimate “brainless” card for medical bills, car repairs, online shopping, and taxes.

Capital One Venture X

- The Reward: 2x miles on every purchase.

- Why it Wins: If you want a premium travel card that also serves as a daily driver, this is it. Instead of earning 1x on random expenses like most premium cards, the Venture X gives you a high 2x floor, making it the perfect everyday card for high-spenders.

2. The Foodie: Best for Groceries and Dining

For the average household, food (both eating out and cooking at home) is the second-largest expense after housing. You need an everyday credit card that treats food as a VIP category.

American Express® Gold Card

- The Reward: 4X points at restaurants worldwide and U.S. supermarkets (up to $25,000 per year in purchases, then 1X).

- Why it Wins: Despite its higher annual fee (now $325), the Amex Gold is mathematically unstoppable if you spend heavily on food. The monthly dining and Uber credits heavily offset the fee, making it a lucrative daily driver for urban professionals.

Capital One Savor Cash Rewards

- The Reward: 3% cash back on dining, entertainment, popular streaming, and at grocery stores.

- Why it Wins: With no annual fee, this is the most accessible lifestyle card on the market. Earning an unlimited 3% back on your Friday night takeout and Sunday morning grocery run is pure profit.

3. The Commuter: Best for Gas and Transit

If you have a long commute or manage a household with multiple vehicles, the pump is draining your cash flow.

Blue Cash Preferred® Card from American Express

- The Reward: 3% cash back on U.S. gas stations and transit (including rideshares, parking, and tolls), plus a massive 6% back at U.S. supermarkets (up to $6,000 per year).

- Why it Wins: While it has a $95 annual fee (often waived the first year), maxing out the 6% grocery category yields $360, while the uncapped 3% on gas and transit secures your daily commute.

4. The 2026 Trend: Mobile Wallet Multipliers

One of the biggest shifts in the 2026 credit landscape is the rise of the “Digital Swipe.”

U.S. Bank Altitude® Reserve Visa Infinite® Card

- The Reward: 3x points on eligible travel and mobile wallet purchases (Apple Pay, Google Pay).

- The Strategy: Because almost every grocery store, gas station, and retail shop accepts contactless payment in 2026, this card essentially becomes a 3x flat-rate card for your in-person everyday spending. If you redeem those points for travel, they are worth 1.5 cents each, giving you an effective 4.5% return on your daily coffee and groceries.

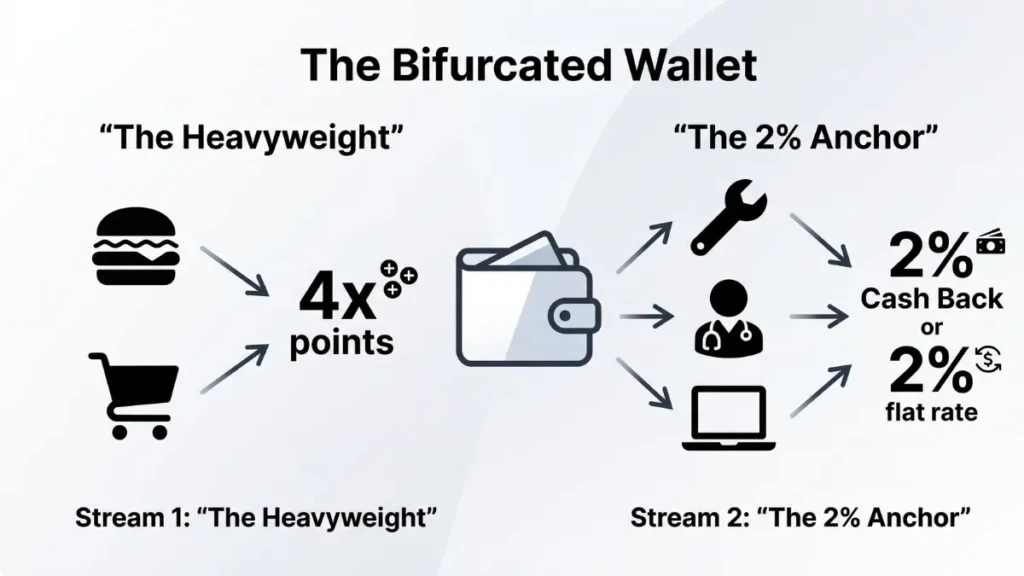

5. Strategic Playbook: The “Bifurcated” Wallet

To achieve maximum efficiency without overwhelming yourself, use the two-card “Bifurcated” strategy:

- The Category Heavyweight: Use a card like the Amex Gold or Capital One Savor exclusively for food and entertainment to capture those 3x-4x multipliers.

- The 2% Anchor: Keep a flat-rate card (like the Citi Double Cash) directly behind it in your wallet. Use this card for literally everything else (pharmacies, hardware stores, vet bills) so you never earn less than 2%.

Expert Insight: Beware the “Caps”

We spoke with a certified financial planner about the biggest trap consumers fall into when choosing a daily driver.

“People get blinded by the ‘6% Cash Back’ marketing, but they fail to read the fine print. Most ultra-high multiplier cards have strict annual spending caps. If a card offers 5% back on groceries but caps it at $1,500 a quarter, a family of four will hit that limit in five weeks. After that, they are earning a miserable 1% for the rest of the quarter. Always calculate your actual monthly spend against the card’s limits before you apply.”

Frequently Asked Questions (FAQ)

What is an “everyday” credit card?

An everyday credit card is designed to reward the purchases you make routinely. Instead of focusing on airline miles or hotel statuses, these cards prioritize multipliers in categories like groceries, gas, dining, and transit, or they offer a high flat-rate return on all purchases.

Should I use my travel card for everyday spending?

Unless your travel card has a high flat-rate baseline (like the Venture X at 2x), you should not use it for un-categorized daily spend. Putting a $1,000 car repair on a Chase Sapphire Preferred only earns you 1,000 points. Putting it on a 2% cashback card earns you a guaranteed $20.

Is an annual fee worth it for an everyday card?

It is only a math equation. If an everyday card charges a $95 fee but offers 6% back on groceries, and you spend $5,000 a year on groceries, you earn $300. Subtract the $95 fee, and you are ahead by $205. If a no-fee card only earns 2% ($100), the fee card is mathematically superior.

Does leaving a small balance on my everyday card build credit faster?

No. This is a persistent and toxic financial myth. Leaving a balance on your card does absolutely nothing to boost your credit score; it only subjects you to high interest charges. Always pay your statement balance in full, every single month.

Stop Swiping for 1%

The money you spend on daily logistics is the foundation of your financial life. Every time you swipe a debit card or a basic 1% credit card at the grocery store, you are letting inflation win. By identifying where your money naturally flows and matching it with the right everyday credit card, you turn your daily routine into an automatic wealth-building machine.

Related Post:

How to Avoid Credit Card Interest Completely in 2026

15th Apr 2026[…] Best Everyday Credit Card 2026: Maximize Your Daily Spend […]