English

English

Best No Annual Fee Credit Cards 2026: The High-ROI Strategy

In the high-stakes world of North American personal finance, there is a persistent myth that you have to pay a premium annual fee to access elite rewards. While a $695 metal card might offer luxury airport lounges, the mathematical reality for most daily spending is that no annual fee credit cards often provide a superior Return on Investment (ROI).

When you pay a $95 or $250 annual fee, you are starting the year at a “financial deficit.” You have to spend thousands of dollars just to break even before you earn a single cent of actual profit.

In 2026, the market for “free” credit cards has become hyper-competitive. Banks are offering massive 5% multipliers and 2% flat-rate “anchors” with zero membership costs. If you are looking for the best free credit cards USA, you need to stop looking at them as “basic” and start looking at them as precision tools for your cash-flow system.

Here is the analytical breakdown of the top no annual fee credit cards for 2026 and how to structure them for maximum profit.

Table of Contents

- The 2% Anchor: Best Flat-Rate No-Fee Cards

- The Lifestyle Specialist: Best for Groceries & Dining

- The Tech Hack: Best for Mobile Wallet Spending

- The “Travel Lite” Strategy: No-Fee Travel Rewards

- Expert Insight: The “Hidden” Cost of Free Cards

- Frequently Asked Questions (FAQ)

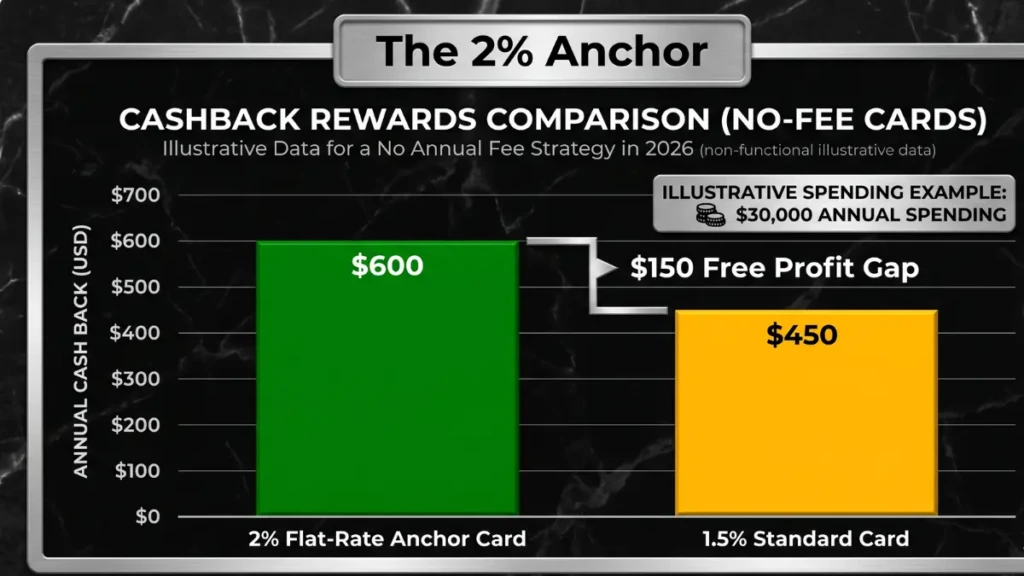

1. The 2% Anchor: Best Flat-Rate No-Fee Cards

Every high-performance wallet needs an “Anchor”—a card you use for every random expense that doesn’t fall into a specific category. In 2026, any card earning less than 2% is a waste of your data.

Wells Fargo Active Cash® Card

- The Reward: Unlimited 2% cash rewards on purchases.

- The Benefit: No categories to track and no caps. It is the ultimate “set it and forget it” tool for your business logistics or personal miscellaneous spend.

- Sign-up Bonus: Typically $200 after spending $500 in the first 3 months.

Citi Double Cash® Card

- The Reward: 1% when you buy, 1% when you pay.

- The Benefit: This card encourages the exact high-performance habit we preach: paying your statement in full. It converts your daily logistics into a predictable revenue stream.

2. The Lifestyle Specialist: Best for Groceries & Dining

If you want to increase credit score quickly while maximizing rewards, you must match your card to your highest “burn rate” categories. For most Americans, that is food.

Capital One Savor Cash Rewards

- The Reward: 3% cash back on dining, entertainment, popular streaming services, and at grocery stores.

- The Strategy: This is arguably the best “daily driver” in the USA for 2026. It captures the bulk of a modern lifestyle’s expenses with a high 3% yield and $0 annual fee.

Chase Freedom Flex®

- The Reward: 5% cash back on up to $1,500 in combined purchases in bonus categories each quarter (requires activation).

- The Strategy: This is a “Tactical” card. While it requires more work to track rotating categories, the 5% ROI on things like Amazon, Gas, or Groceries is unbeatable for a free card.

3. The Tech Hack: Best for Mobile Wallet Spending

The “hidden truth” of 2026 is that the physical card is becoming obsolete. If a merchant accepts Apple Pay or Google Pay, you should be using a card optimized for digital swiping.

U.S. Bank Altitude® Go Visa Signature® Card

- The Reward: 4X points on dining (including takeout and delivery) and 2X points at grocery stores, gas stations, and streaming services.

- The Benefit: Because it offers a $15 annual streaming credit and high food multipliers, it is the perfect companion for a digital-first professional.

4. The “Travel Lite” Strategy: No-Fee Travel Rewards

You don’t need a $395 Venture X to earn travel miles. If you travel once or twice a year, these no annual fee credit cards offer the protection and rewards you need without the overhead.

Wells Fargo Autograph℠ Card

- The Reward: 3X points on restaurants, travel, gas, transit, and popular streaming services.

- The “Secret” Perk: It includes Cell Phone Protection (up to $600) just for paying your monthly bill with the card. This is a premium-tier benefit on a $0 fee card.

Expert Insight: The “Hidden” Cost of Free Cards

We consulted a consumer credit analyst about the psychological trap of “no-fee” banking.

“The biggest mistake people make with best free credit cards USA is assuming ‘no fee’ means ‘no cost.’ Banks make their money on these cards through high interest rates and ‘Foreign Transaction Fees.’ If you take a standard no-fee card to Europe or Canada and spend $5,000, you will likely be hit with a 3% surcharge ($150). That is more expensive than many annual fees. Always check for the ‘No Foreign Transaction Fee’ label if you plan to use the card globally.”

Frequently Asked Questions (FAQ)

Are no annual fee credit cards actually free?

Yes, as long as you pay your statement balance in full every month. There is no membership cost to hold the card. However, if you carry a balance, you will be charged interest (APR), which is how the banks profit from these cards.

Which no-fee card is best for building a credit score?

If you have “Fair” credit, the Capital One Platinum or Discover it® Secured are excellent no-fee options. They report to all three credit bureaus, allowing you to build the history needed to graduate to the high-multiplier 2% and 5% cards.

Can I get a sign-up bonus on a card with no annual fee?

Absolutely. Many cards in the 2026 market offer “Introductory Bonuses” ranging from $150 to $200. This is essentially the bank paying you to try their product. It is a pure 100% ROI on your initial spending.

Do these cards have foreign transaction fees?

Most do. However, cards like the Capital One Savor and the Wells Fargo Autograph are rare exceptions that offer $0 annual fees and $0 foreign transaction fees, making them the ultimate global logistics tools.

What is the “catch-all” card strategy?

This involves carrying one card with a high flat rate (like 2% on everything) for random purchases, and a second card with high multipliers (like 3-5% on groceries) for specific spending. This “Bifurcated Wallet” ensures you never earn just 1% on any transaction.

Is it better to have one premium card or three no-fee cards?

Mathematically, three no-fee cards often yield more cashback. However, a premium card (like the Venture X) provides non-monetary value like airport lounge access and primary rental car insurance. For pure cash-flow optimization, the no-fee route is usually superior.

How many no-fee cards should I have?

To maximize your FICO score and your rewards, having 3 to 5 no-fee cards is optimal. This increases your total available credit, which lowers your credit utilization ratio and provides multiple category multipliers for different types of spending.

Do no-fee cards offer travel insurance?

Some do, but it is typically “Secondary” coverage. This means it only kicks in after your personal auto or travel insurance. For “Primary” coverage, you usually have to move into the $95+ annual fee tier.

Command Your Cash Flow

In 2026, the most sophisticated spenders are those who refuse to pay for things that should be free. By anchoring your wallet with a 2% flat-rate card and specializing with food and tech multipliers, you build a high-yield financial system with zero overhead. Stop paying the “annual fee tax” and start extracting the maximum ROI from your daily routine.

Ready to ensure your credit score is high enough to qualify for these top-tier cards? Follow our 30-day blueprint: [How to Improve Credit Score Fast in 30 Days (2026 Guide)].