English

English

Hidden Credit Card Fees You’re Probably Paying (And How to Avoid Them)

The modern credit card is a masterclass in behavioral psychology. Banks lure you in with promises of 5% cash back, massive sign-up bonuses, and premium airport lounge access. But these massive corporate rewards programs aren’t funded by charity; they are funded by the millions of consumers who fall into the trap of the fine print.

If you are treating your credit card like a debit card, you are likely leaking hundreds of dollars a year in penalty charges and administrative costs. The banking industry relies on “frictionless spending” to make you gloss over the Schumer Box—the standardized chart where all the real costs are legally buried.

If you want to keep your cash flow optimized in 2026, you must play the game on your terms. Here are the 5 most expensive hidden credit card fees you are probably paying right now, and the exact operational steps to avoid them completely.

Table of Contents

- The Dynamic Currency Conversion (DCC) Trap

- The Cash Advance Catastrophe

- The Deferred Interest “Time Bomb” (Store Cards)

- The Balance Transfer Illusion

- Expert Insight: The Grace Period Illusion

- Frequently Asked Questions (FAQ)

1. The Dynamic Currency Conversion (DCC) Trap

This is the most common hidden fee for international travelers and online shoppers buying from overseas vendors.

When you swipe your card in Europe, Canada, or Mexico, the credit card terminal will often ask a seemingly helpful question: “Would you like to pay in US Dollars (USD) or the local currency?”

Your brain naturally wants to select USD because it is familiar. Do not do it. * The Trap: If you select USD, you are agreeing to Dynamic Currency Conversion (DCC). The foreign merchant’s bank gets to choose the exchange rate, which is almost always terrible, and they bake a hidden 3% to 7% markup directly into the price.

- How to Avoid It: Always, without exception, choose to pay in the local currency. Let your own credit card company handle the conversion. As long as you are using a card with “No Foreign Transaction Fees,” you will get the pure, wholesale exchange rate with zero markup.

2. The Cash Advance Catastrophe

Credit cards are designed to buy things, not to buy money.

If you take your credit card to an ATM and withdraw cash, or use it to buy lottery tickets or casino chips, you trigger a Cash Advance.

- The Trap: A cash advance is the most toxic transaction you can make. First, you are hit with an upfront fee (usually 5% of the amount withdrawn). Second, the interest rate for a cash advance is typically 5% to 10% higher than your normal purchase APR. Finally—and worst of all—there is no grace period. Interest begins compounding the absolute second the ATM hands you the cash, even if you pay your bill in full at the end of the month.

- How to Avoid It: Never put a credit card inside an ATM. If you need liquid cash, use a debit card. Keep your credit cards strictly for point-of-sale transactions.

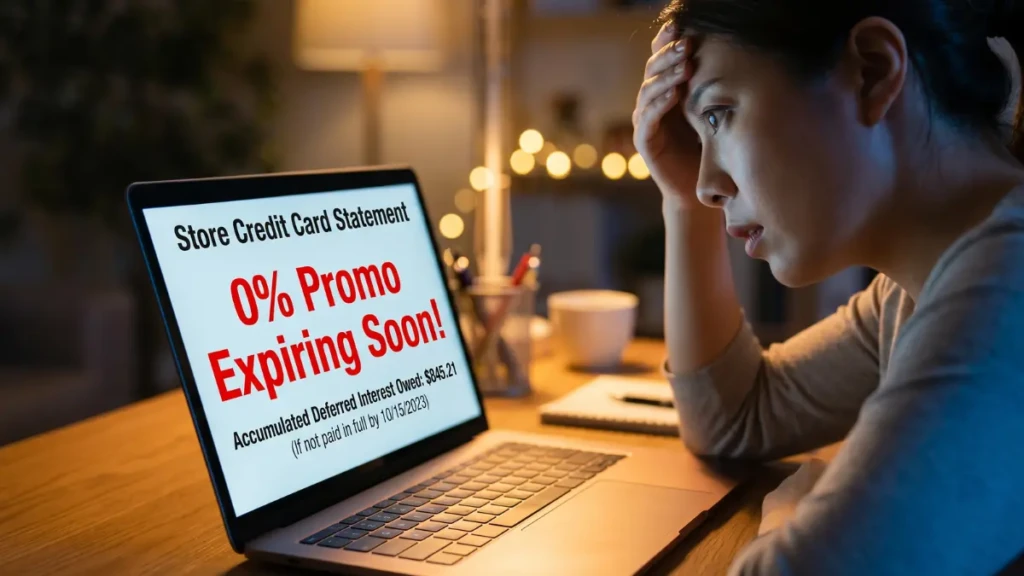

3. The Deferred Interest “Time Bomb” (Store Cards)

You are checking out at a major electronics or furniture store, and the cashier offers you “0% Interest for 12 Months” if you open their store card today.

- The Trap: Most store cards do not offer true 0% APR; they offer Deferred Interest. This means interest is still accumulating silently in the background at an absurd rate (often 29.99%). If you pay off the TV in 11 months, you pay zero interest. But if you have even a $1 balance left on day 366, the bank retroactively hits your account with all the interest that accumulated over the entire year. A $1,000 TV instantly becomes a $1,300 TV.

- How to Avoid It: If you use a deferred interest promo, divide the total purchase price by 11 (not 12). Set up automated payments to ensure the balance is eradicated a full month before the promotional period officially ends.

4. The Balance Transfer Illusion

When you are drowning in high-interest debt, moving that balance to a new card offering “0% APR for 18 months” seems like a brilliant financial rescue plan.

- The Trap: The interest might be 0%, but the transfer itself is not free. Buried in the fine print is a Balance Transfer Fee, which is usually 3% to 5% of the total amount moved. If you transfer $10,000 to escape high interest, the bank instantly tacks $500 onto your principal balance just for processing the transaction.

- How to Avoid It: You cannot always avoid this fee, but you must calculate the math. If transferring saves you $1,500 in interest over the year, paying a $300 upfront fee is mathematically sound. However, actively seek out credit unions or specific promotional cards that explicitly offer “$0 Balance Transfer Fees” during the first 60 days of account opening.

Expert Insight: The Grace Period Illusion

We asked a former credit card underwriting executive about the biggest misconception consumers have regarding their monthly statements.

“People think the ‘Grace Period’—the 21 days you have to pay your bill before interest hits—is a permanent right. It isn’t. If you carry a balance from month to month, even just $10, you immediately forfeit your grace period for the next billing cycle. This means any new purchase you make tomorrow will start accruing daily interest the moment you swipe the card. The only way to restore your grace period and avoid these hidden credit card fees is to pay your statement balance to absolute zero for two consecutive months.”

Frequently Asked Questions (FAQ)

What is an over-limit fee and do cards still charge it?

In the past, if you tried to spend past your credit limit, the transaction would go through, but the bank would hit you with a massive $35 penalty. Thanks to recent consumer protection laws, banks can no longer automatically charge over-limit fees unless you explicitly “opt-in” to allow your card to go over the limit. Simply do not opt-in. If you don’t have the limit, the card will just decline (which is free).

How do I find out what fees my card charges?

Search online for your specific credit card name followed by “Schumer Box” or “Terms and Conditions.” The Schumer Box is a federally mandated, standardized table that must clearly list the Annual Fee, APR, Penalty APR, Cash Advance fees, and Foreign Transaction fees in an easy-to-read format.

Is it worth paying an annual fee?

It is only worth paying an annual fee if your organic spending generates more value than the fee costs. If you pay a $95 annual fee but the card gives you $300 a year in grocery cash back that a free card wouldn’t, the fee is mathematically justified. If you aren’t doing the math, downgrade to a free card.

Can I get a late fee waived?

Yes. If you have a historically strong record of paying on time and accidentally miss a payment by a day or two, call the number on the back of your card. Customer service representatives are generally authorized to waive one late fee per year as a courtesy to keep your business. You just have to ask.

Plug the Financial Leaks

The banking system is designed to reward the disciplined and penalize the unaware. By understanding the mechanics of DCC, avoiding the cash advance trap, and respecting the danger of deferred interest, you neutralize the banks’ most profitable tricks. Stop paying for their corporate retreats and start keeping your capital where it belongs: in your own accounts.

To ensure you are using the right tools in your wallet, check out our master breakdown on the [Best No Annual Fee Cashback Cards: The 2026 Strategy Guide].