English

English

Best No Annual Fee Credit Cards in the USA (2026 Guide)

In the modern financial landscape, paying an annual fee for a credit card is often a mathematical error. While premium $695 metal cards offer flashy perks like airport lounge access, the vast majority of consumers and founders end up losing money because their organic spending never offsets the upfront cost.

When you strip away the marketing, the goal of a credit card is simple: to act as a frictionless payment mechanism that generates a positive Return on Investment (ROI) on the money you are already spending.

If you want to optimize your financial logistics in 2026, no annual fee credit cards are your most powerful asset. You start the year at a pure $0 deficit, meaning every point, mile, or cent of cash back you earn is pure profit. Here is the analytical breakdown of the absolute best no-fee cards in the USA and how to structure them for maximum yield.

Table of Contents

- The Baseline: The 2% Flat-Rate Anchor

- The Lifestyle Multiplier: Groceries & Dining

- The Strategic Maximizer: Rotating 5% Categories

- Expert Insight: The “No Foreign Transaction Fee” Loophole

- Frequently Asked Questions (FAQ)

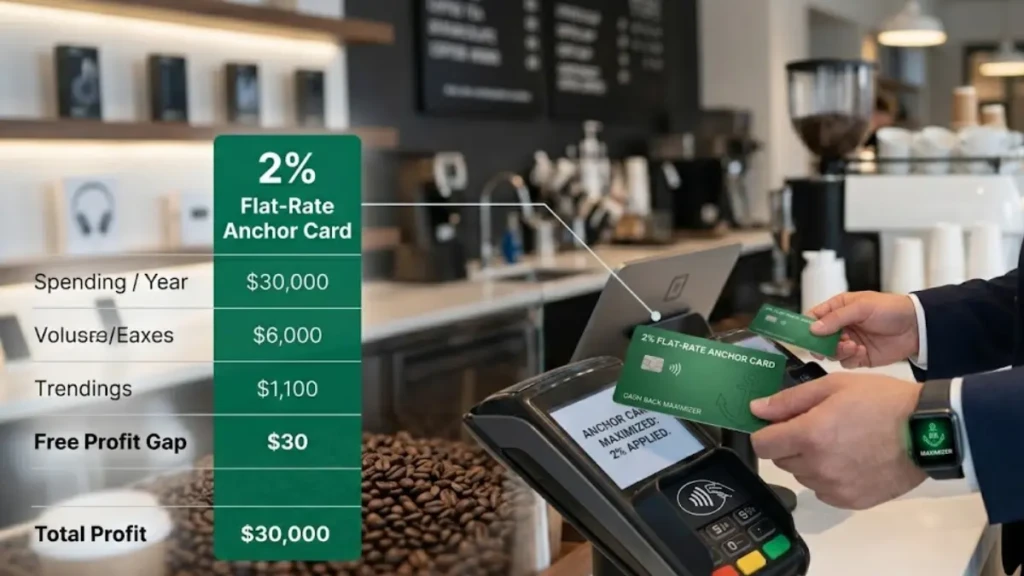

1. The Baseline: The 2% Flat-Rate Anchor

Every high-performance wallet requires an “Anchor Card.” This is the card you pull out for random, uncategorized expenses like a mechanic bill, a software subscription, or dental work. If your anchor card earns less than 2%, you are leaving capital on the table.

Citi Double Cash® Card

- The Mechanics: You earn 1% cash back when you swipe, and another 1% when you pay your bill.

- The Value: This card enforces the ultimate financial habit: paying your statement in full. It turns every miscellaneous business expense or personal purchase into an automatic 2% discount with zero caps.

Wells Fargo Active Cash® Card

- The Mechanics: A straightforward, unlimited 2% cash rewards rate on all purchases.

- The Value: If you prefer instant gratification over the “pay to earn” model of the Citi card, the Active Cash is the definitive set-it-and-forget-it card for 2026. It typically includes a strong sign-up bonus, offering an immediate cash injection.

2. The Lifestyle Multiplier: Groceries & Dining

Once your 2% baseline is established, you need a specialized card for your highest “burn rate” categories. For the vast majority of Americans, this is food and entertainment.

Capital One Savor Cash Rewards

- The Mechanics: Earns a massive 3% cash back on dining, entertainment, popular streaming services, and at grocery stores.

- The Value: This is arguably the best “daily driver” among no annual fee credit cards. It captures the core of a modern lifestyle. Whether you are buying groceries for the week or paying for a client dinner, you are consistently generating a 3% yield with absolutely zero category tracking required.

3. The Strategic Maximizer: Rotating 5% Categories

If you are willing to exert a tiny bit of effort to track a calendar, you can push your rewards rate into the elite 5% tier without paying an annual fee.

Chase Freedom Flex®

- The Mechanics: Earns 5% cash back on up to $1,500 in combined purchases in bonus categories each quarter you activate (like Amazon, gas stations, or wholesale clubs). It also provides a permanent 3% on dining and drugstores.

- The Value: The Freedom Flex is a tactical card. When the 5% category aligns with your current logistics (e.g., a massive Amazon run for office supplies during Q4), it provides an unbeatable return. Furthermore, if you later upgrade to a premium Chase card, these points can be transferred to travel partners for even higher valuations.

Expert Insight: The “No Foreign Transaction Fee” Loophole

We asked a global digital operator what the biggest mistake consumers make with “free” cards.

“Most people think ‘no annual fee’ means ‘totally free.’ It doesn’t. If you take a standard free card to Europe or Canada and spend $5,000, you will likely be hit with a hidden 3% Foreign Transaction Fee, which costs you $150. That is more expensive than many annual fees. If your income is global or you travel frequently, you must ensure your card explicitly waives this fee. The Capital One Quicksilver and Capital One Savor are rare, powerful exceptions that offer zero annual fees and zero foreign transaction fees.”

Frequently Asked Questions (FAQ)

Can I get a sign-up bonus on no annual fee credit cards?

Yes. In 2026, the market is highly competitive. Cards like the Chase Freedom Flex and Wells Fargo Active Cash routinely offer introductory bonuses ranging from $150 to $200 after you spend a small threshold (usually $500) in the first three months. This is a 30% to 40% immediate ROI on your initial spending.

Are these cards good for building a credit score?

If you already have “Good” to “Excellent” credit (670+), these cards are perfect for maintaining and growing your score by lowering your credit utilization ratio. If you are starting from scratch or rebuilding, you should look for “Secured” no-fee cards, like the Discover it® Secured, which are specifically designed to establish a credit history.

What is the “Bifurcated Wallet” strategy?

This is the optimal setup for cash flow. You carry exactly two cards: a 2% flat-rate card (like the Citi Double Cash) for general spending, and a 3% multiplier card (like the Capital One Savor) for high-spend categories like food. This ensures that every single dollar you spend is returning a minimum of 2% to 3%, far outperforming a single-card setup.

Command Your Capital

Banks rely on you ignoring the math. By cutting out the annual fee and utilizing a strict 2% to 5% cash back strategy, you turn your everyday logistics into a predictable revenue stream. Pick the no annual fee credit cards that match your highest spending categories, set them to auto-pay, and let the systems generate your profit in the background.

To ensure your credit file is robust enough to instantly qualify for these cards, read our tactical guide: [How to Improve Credit Score Fast in 30 Days (2026 Guide)].

This video breaks down the top cash back cards currently available, many of which are no-fee options that align perfectly with a high-ROI financial strategy.